If you had to “show” your personal financial plan right now, what would you open:

- your bank app,

- a stray spreadsheet,

- or… nothing?

If your money feels scattered or you’re living off vibes and balances, this guide is your reset.

I’m walking you through exactly how I rebuilt my personal finance stack this year as a CPA who lives and breathes numbers for a living … what I switched to, why, and how to set it up in an afternoon.

Quick links to jump in:

- Try Crew (personal banking) + APY boost → jamietrull.com/crew

- Get 50% off Year 1 of Monarch (budgeting) → jamietrull.com/monarch

Why Most Personal Money Systems Break

(Even for “Numbers” People)

- Bank-only “budgeting” isn’t budgeting. A running balance can’t tell you if you’re on track for travel, braces, or replacing the car next year.

- Spreadsheet drift is real. Great in January—abandoned by March. If it isn’t automatic, it won’t be consistent.

- Couple coordination gets messy. One partner tracks, the other transacts. Without shared visibility and alerts, overspending is inevitable.

- Kids + money = mystery. You want to teach them. You also want guardrails. Few banks make that easy—especially if you pay your kids from a family business.

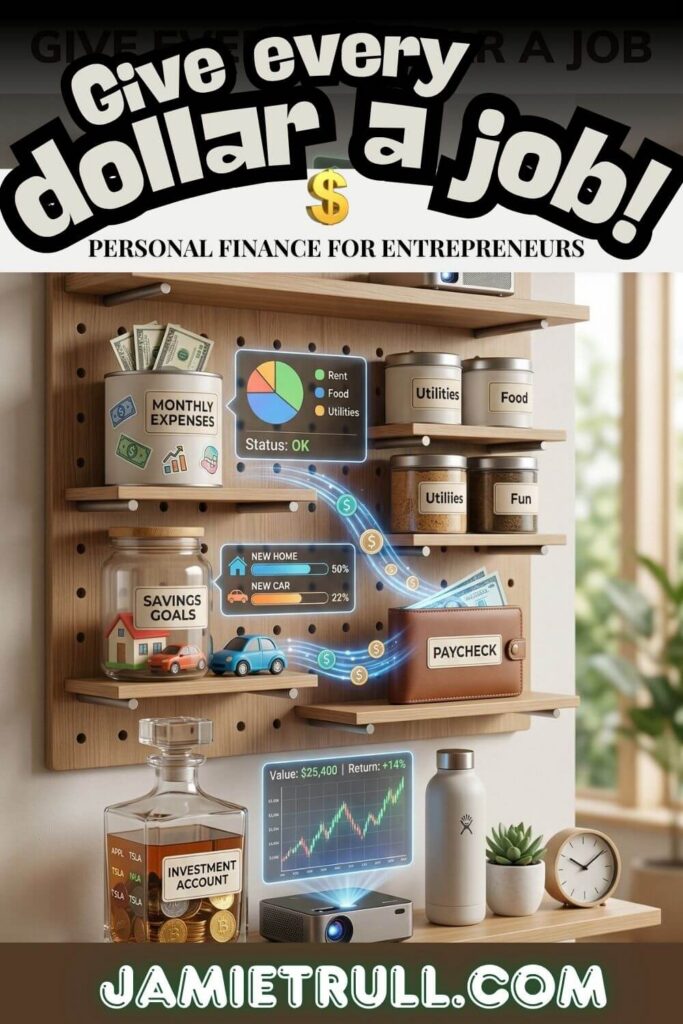

I wanted a system that was automatic, visual, collaborative, and forgiving. That’s why I split the job between two tools:

- Crew for smart banking (high-yield checking, savings “pockets,” family accounts, automation).

- Monarch for comprehensive budgeting & planning (net worth, cash flow, category rules, shared goals).

What A “Good” Personal Money Operating System Looks Like

- One primary bank you actually like: fast transfers, useful automations, sub-accounts/pockets, and interest that isn’t a joke.

- One budgeting hub that pulls in every account, auto-categorizes, alerts you early, and shows progress toward goals.

- Weekly 20-minute ritual to make tiny course corrections (not giant April freak-outs).

- Automated savings & bills so “best behavior” happens by default.

- Simple family setup so kids can learn and you can see everything without running to a branch.

Part 1: Why I Switched My Personal Banking to Crew

I’ve had a big-name bank for almost two decades. It was fine—until I realized “fine” was costing me time, interest, and clarity. Crew (a fintech that partners with an FDIC-insured bank) won me over with three things:

1) High-Yield Checking (Not Just Savings)

Most “high-yield” offers hide behind savings accounts with withdrawal rules. Crew pays a market-leading APY on checking, so my everyday money actually earns. That means bill-pay cash, emergency cash, and short-term goal cash don’t sit idle. Pair that with the APY boost via my link and it’s a no-brainer for parked dollars you’ll still use.

How I use it:

- Keep one month of expenses + bills in the main checking balance.

- Keep 3–6 months of expenses in an emergency pocket (still earning).

- Park upcoming “big rocks” (insurance, annual travel, property tax) in their own pockets.

2) Pockets (Savings Buckets) + Automations

Crew lets you create labeled pockets (mini-accounts) and set rules that move money automatically when your paycheck hits.

My rules:

- 30% → Taxes/Annuals pocket (insurance premiums, property tax, etc.)

- 10% → Travel pocket

- 10% → Car replacement pocket

- 5% → Giving pocket

- 5% → Kids pocket

- Remainder stays in checking for bills & variable spending

I don’t “try” to save—I already saved when the deposit landed.

3) Family Accounts That Actually Work

I set up individual accounts for my kids (each with their own account/routing). I can push money in instantly, view activity, and—this is rare—even direct deposit to their accounts. If you legally employ your minor kids in your business (done correctly), this is huge. Even if you don’t, Crew makes an excellent allowance + lessons platform without monthly fees.

Kid workflow:

- Create a “Family” space in Crew.

- Set a weekly allowance rule.

- Add a 10% auto-give and 20% auto-save rule inside their account so they learn to allocate on autopilot.

Getting Started with Crew (10-Minute Setup)

- Open at jamietrull.com/crew and enroll (use code JAMIE if the app asks).

- Add your old bank as a link and pull seed funds into Crew.

- Create pockets: Emergency, Annual Bills, Travel, Car, Kids, Giving (and anything else you need).

- Set automation rules (percent splits) from your next incoming deposit.

- Update bill autopays to Crew over the next week (don’t rush; do the big ones first).

- Keep your old bank as a backup while you transition. No pressure to close it immediately.

Part 2: Why I Moved Budgeting to Monarch Money

RIP Mint. I loved it. But Monarch is the grown-up version with the controls I always wanted.

What Monarch Does Exceptionally Well

- All-in aggregation: Banks, credit cards, loans, investments, even your mortgage and credit score—one dashboard.

- Category rules that stick: Create rules once, Monarch remembers (merchant, amount ranges, notes).

- Split transactions cleanly: One Target run → Groceries + Household + Kids in a few clicks.

- Fixed vs. flexible budgeting: Separate non-negotiables (mortgage, utilities) from adjustable spend (dining, fun, shopping) to see where change is possible.

- Goals & rollovers: Set sinking funds and watch progress. Unused categories can roll forward automatically.

- Cash flow & net worth timelines: See month-over-month spend, income trends, and long-term wealth trajectory (this motivates like nothing else).

- Shared views & alerts: Invite your spouse/partner; both get real-time alerts and a single source of truth.

- Performance & stability: It’s fast, modern, and less glitchy than many rivals.

My Monarch Structure (Steal It)

- Top-level budgets: Housing, Transportation, Food, Health, Kids, Giving, Fun, Personal Development, Subscriptions, Misc.

- Automation:

- Rules: Costco → “Groceries,” Gas station → “Fuel,” Insurance Co. → “Annuals”

- Split recurring orders (e.g., Amazon) so I see the real story, not a giant “Shopping” blur

- Goals:

- Travel 2026 target, New car 2028, Home projects fund

- Reports:

- Cash Flow (last 12 months), Category Trends (Food + Subscriptions), Net Worth timeline

- Alerts:

- Big purchase alert > $500, Bill due alerts, Budget threshold at 80% spent

Getting Started with Monarch (20-Minute Setup)

- Sign up at jamietrull.com/monarch (use the link for 50% off your first year).

- Connect every account (checking, savings, cards, loans, investments).

- Accept the suggested categories, then customize your top 12–15.

- Build your monthly plan: fixed (mortgage, insurance, internet), flexible (dining, fun, shopping).

- Create rules for your top 10 merchants.

- Add 3 goals you care about (with numbers & due dates).

- Invite your partner; turn on alerts.

- Review weekly (see the ritual below).

The Weekly 20-Minute Ritual (Money Monday, Personal Edition)

Every Monday:

- Open Monarch → Notifications first.

- Approve categories (Monarch learns fast if you correct it consistently).

- Check cash flow for last 7 days; scan for surprises.

- Crew pockets check: do you need to top up Travel or Annuals after a big spend?

- Adjust this week’s plan: Move $50 from “Fun” to “Gifts” if a birthday popped up.

- Two-minute Wins: Cancel a dusty subscription; schedule one bill you’ve been avoiding.

- Glance at goals: progress bars = motivation.

That’s it. Twenty minutes prevents end-of-month panic.

The “Buckets + Budget” Playbook

(How It All Clicks)

Crew handles cash (where dollars live and what job they’re doing).

Monarch handles behavior (what those dollars did and whether you’re on plan).

Example: Annual Insurance Premium

- You’ll owe $1,200 next November.

- Crew rule: $100/mo to Annual Bills pocket.

- Monarch: Track the $1,200 as a goal. Each month, progress ticks up automatically from Crew’s transfer. In November, you pay the bill from the pocket—no scramble.

Example: Family Travel

- Crew: $250/mo to Travel pocket.

- Monarch: Add trip as a goal; as you book flights/hotel, categorize them to “Travel: 2026 Europe” so you can see total costs vs. plan.

Example: Teaching Kids Money

- Crew: Kids’ accounts with auto-save and auto-give rules.

- Monarch: Track family-wide spend and add a category “Kids Earned Pay/Allowance” to visualize how often you’re funding it.

30-Minute Quick-Start Plan

(Follow This Checklist)

Minute 0–10: Crew

- Open or log in at jamietrull.com/crew

- Create Emergency, Annual Bills, Travel, Car, Kids, Giving pockets

- Set percent allocations off your next deposit

Minute 10–30: Monarch

- Join via jamietrull.com/monarch (activate 50% off)

- Connect accounts, set categories, add three rules and three goals

- Turn on alerts, invite partner

Then calendar a Money Monday repeating event. Your future self will be obsessed with you.

Troubleshooting & FAQs

Q: Do I have to close my old bank?

A: No. Keep it as a backup. Move direct deposit to Crew when you’re ready and flip autopays over one by one.

Q: I used Mint. Is Monarch worth paying for?

A: If it prevents even one overspend category or catches a duplicate subscription, it pays for itself. The planning and reporting features alone beat what Mint offered.

Q: What about cash envelopes?

A: Crew pockets are the digital envelope system—but safer, automated, and earning interest.

Q: How do I budget as a couple without fights?

A: Use Monarch’s fixed vs. flexible split. Agree that fixed items are non-negotiable. Give each partner a no-questions-asked “Personal Fun” category. Let alerts tell you when “We” spending hits 80% before it’s a problem.

Q: Can my kids really have their own accounts?

A: Yes—Crew’s family setup supports child accounts you can view and fund. It’s fantastic for allowance, savings habits, and (if applicable) properly paid wages from a family business.

Q: What about safety?

A: Crew is a fintech layered on an FDIC-insured bank partner, combining modern features with deposit protection up to legal limits.

Your Personal Finance Flywheel (What Happens After 90 Days)

- Clarity: You’ll know where your money actually goes—and your net worth line will finally tell a story.

- Momentum: Automations will do the heavy lifting; your weekly ritual will keep you honest.

- Calm: Big, scary annual bills become just another Tuesday because the pocket is ready.

- Confidence: You’ll make better decisions because the numbers are visible—and simple.

Ready to Copy My Setup?

- Open Crew (high-yield checking + pockets + family accounts) → jamietrull.com/crew

- Get Monarch (budgeting, net worth, cash flow, goals) with 50% off Year 1 → jamietrull.com/monarch

Set it up once. Let it run. Check in weekly. That’s the whole game.

Sponsor & Affiliate Disclosures

Some links in this post are partner/affiliate links. If you click and purchase, I may receive a commission or bonus at no additional cost to you. I only recommend tools I use personally or have vetted for real utility.

This article is for educational purposes only and not financial, tax, or legal advice. Your situation is unique—consider consulting a qualified professional for personalized guidance.

This transcript was generated from the video for your convenience, but it may contain typos or slight errors due to the transcription process. For the most accurate and complete information, we recommend watching the full YouTube video.

How to organize personal finances and manage your finances effectively

Now, be honest. If someone asked you to explain your personal financial plan right now, what would you point to? Would it be a spreadsheet, maybe a notes app or a bank account, or maybe just pure vibes if your money system feels scattered or maybe doesn’t even exist at all? This video is for you. Hi everyone.

I’m Jamie Trull, CPA, and financial Educator, and typically on this channel, I’m bringing you all the things you need to stay informed. Organized and profitable in your business finances. But today I’m gonna diverge a little bit and we’re gonna talk about personal finances, and that’s because as self-employed individuals, small business owners, entrepreneurs, we also have personal finances we need to worry about.

And while they are separate things. At least they should be. They also have quite a bit of overlap. Now, in 2025, I decided to switch all the tools I was using for my business finances, and I recently made a video all about that. So go check that out next. But when making that video, I also realized I had made a lot of changes in what I was using on the personal side of the finance house as well.

So this video is gonna be about those changes that I made. What I’m using now and why, and specifically in this video, I’m gonna be talking about switching my personal banking solution and also switching my budgeting solution. Plus I’m gonna show you a little bit of behind the scenes as to how these tools actually work so that you can decide if they will be a good fit for you.

Choosing accounts regularly based on your financial goals and monthly income

So the first thing I decided to switch was my personal banking platform. Now, I don’t know about you, but I have had the same personal bank for going on 20 years now. It has been a long time since I even thought about switching, and I haven’t had a particularly negative experience with it. I use a big bank.

It has branches that I can go walk into or go withdraw cash from. I really like that and I’ve never really spent a lot of time researching. Other personal banking solutions that could work for me. To be honest, I kind of just assumed they were all sort of the same. But what I realized actually, once I started digging into this a little bit, is that I was missing out on a lot of really cool features that you can find in some of these banking solutions that my big bank.

Does not offer. So I started surveying some friends of mine who are really big in the personal finance space, asking them what they use. ’cause I know they have done a lot of the digging and the research. And so I had a handful of things to go check out based on their very sage advice. And at the end of the day, I decided to settle on.

Crew. Now Crew, very similar to Relay, which I use for business banking, is actually a FinTech, and that means that they themselves aren’t a bank, they’re a financial technology company, but they partner with an FDIC insured bank. On the flip side of that, being a FinTech also means that pretty much everything is done digitally.

Using a high yield account and building an emergency fund with a smart filing system

They don’t have branches that you can go. Walk into and talk to someone. So that’s a consideration when you are looking at various different personal accounts. Personally, I decided to keep my longstanding relationship with my big bank to have that bank to still be able to utilize if I choose to. But now I’ve added crew to my personal tech stack, and there are three main reasons that I decided on crew.

The first reason is the biggest one, and that is that it was the only account that I could find that offered high interest. Check it and notice that I said checking, not savings. You can find various different high yield savings accounts that are gonna have rules on how you withdraw the money, but this is actually a high yield checking account, and that means I can use it just like a regular checking account and still be able to be earning interest at all times on the money that is in there.

And you might assume that since it’s a checking account, it probably doesn’t come with as high yield. Of interest rates as maybe some of your HSAs do, and you would be wrong. When I went and compared it, actually the rates that crew had were higher than a lot of the other banks that I looked at. So that for me was an immediate yes, that was absolutely.

Huge. The second thing that I absolutely love about Crew is that it has a very similar ability to why I love Relay for business banking, which is because you can actually have separate different buckets that you’re putting your money into and have automations for.

Creating a monthly budget and organizing monthly expenses with automation

That crew has that as well. They call it their pocket functionality, and so you can actually put money into various different pockets if you’re saving for different goals and you can automate money going from your regular checking. Into those various different pockets. So that’s such a great way to be able to set up and make progress that is really, really visible toward the goals that you have. So whether you are trying to save up for a new car, or maybe for that next vacation, you can actually set up various different pockets and the money can automatically, or you can do it yourself, be pulled into these various different pockets and all of the sudden you now have.

Accidentally saved your way into meeting your goals. And if y’all know me, you know that I am a huge fan of automations and I love being able to separate out your money and give your money a job. In fact, I actually teach a methodology for business called profit planning. You can grab my free profit plan template at the link below, but ultimately, I love the ability to give every dollar a job, and that’s the exact same thing that you can do in.

Crew. And the third thing that I loved about Crew, and I actually didn’t even know this until I got set up in crew and realized how amazing it was. They have the capability for family accounts. And if you watch any of my content, you know how big I am on teaching your kids young, how to use money, how to save money.

Managing your finances with family accounts and financial documents organization

Right How to give money. All of that is really important to their growing into a responsible human being that knows how to use cash. And I have tons of content out there also about hiring your kids in your business. So if you are a business owner, this is something you uniquely can do and it is such a great way to be able to build wealth for your kids and set them up for success.

So I immediately set up both my kids with crew accounts. They have their own account and routing numbers. They can log in on their device. If they want to, I can see it all on my device and put money into it or take money out of it. And with crew, you can even direct deposit into children’s accounts. So that was something that was really hard to find.

I didn’t realize how hard it would be to find accounts where you could direct deposit into a child’s account who’s under the age of say, 12 or 14. A lot of banking institutions don’t allow for that because they aren’t set up for business owners who may be paying their minor kids, right? And so I advocate for you to use a payroll service and actually pay your kids just like you would any other employee.

But that was a bit of a roadblock for some people who were looking to hire their kids. So this is a great solution also for family banking for anyone who is.

Building financial goals with the right investment account and budgeting tools

Hiring your kids. I previously talked about Greenlight, and while I do still like Greenlight, what I love is that crew has a lot of the same features, but without an account fee.

So that’s absolutely huge that you aren’t having to pay a fee to have an account with crew. So just to sum it up. I absolutely love crew and decided to move there because of the fact that I can do high yield checking, which is amazing. I’ve never seen anybody else offer that. They also have automations and you can put your money into various pockets in order to save for specific things, and I love that they have the ability to do family accounts, so my kids have their accounting crew.

I can view everything in there and we can use that as a great teaching tool. And again, they’re gonna earn interest as well. So overall. I gotta be honest, I’m a little smitten with it so far, and if you wanna try it out, of course, of course, of course. I’ve negotiated a special deal just for you. So go to jamietrull.com/crew, or you can use the QR code that is on the screen.

Or if you already have downloaded the app, you can use the code, Jamie, J-A-M-I-E when you sign up. And if you use any of those methodologies to sign up, you’re gonna get half a percentage boost in your A PY for three months.

How to create a budget and track monthly expenses with budgeting software

So that means your interest rate that you’re earning on that amount that’s in your checking account is going to get boosted by half a percent for a full three months, which depending on how much money you put in there, could actually add up to quite a chunk of change.

So if you decide to try crew, definitely go and use my link to do it. And like I said, you don’t have to get rid of your regular bank. You can use these in tandem. That’s what I’m doing for now. I have a feeling eventually I’ll probably move everything over to Crew, but it can take a little bit of time. So don’t feel pressure that you need to move everything all at once.

You can get started by even just moving over some of your emergency funds into crew, and it’s a great way to kind of segregate that money out and make sure that you don’t spend it while also earning interest on it. So now let’s move on to the second tool that I’m using. So I not only switched my personal banking.

But I also switched over my personal budgeting software this year. Now again, for years and years, I used the exact same budgeting tool. I used the tool from Intuit called Mint, and I gotta give an RIP Mint because about 18 months ago or so, mint went away.

Tracking monthly income and accounts regularly with a powerful budgeting system

And so after I mourned Mint for a little while, I decided it was time to start looking for another. Budgeting software, but I couldn’t find anything similar to Mint and I couldn’t find anything that I liked that also was free.

So after talking to some of the personal finance gurus that I know, they convinced me to take a look at Monarch Money. Now, I kept hearing about Monarch, but I hadn’t looked at it in detail in part because it does have a small account fee each and every month.

And ideally I didn’t want to have that, but. Once I got into Monarch and saw how incredible their functionality was, I realized that I was going to be saving significantly more than their account fee just by being able to have that budgeting software every month and keep tabs of my finances. I’ll tell you in the time that I didn’t have a budgeting software in the in-between.

I definitely overspent in a lot of categories that having a good budget software would’ve prevented. So that helped me get over my mental block of paying for a budgeting software, and I gotta be honest, when I compare it back to Mint, which I did love.

Organizing financial documents and improving your monthly budget strategy

It is heads and tails above it in terms of features and what you can do. The categorization is way better. I can split things between different categories if I want to. I can even split my budget between things that are fixed, things that I can’t really change, like my mortgage and things that are more flexible, things that I have a little bit more control over my spending on.

So it gives a lot of functionality in how you budget, but even more than that, I love. All of the various different reporting that I can get. So y’all know I love to be able to use the numbers in a way that makes sense to be able to see what’s actually happening in my personal finances. So I love being able to track things like my net worth, how did I do on my budgets each and every month?

How much cash came in, how much cash went out. What categories was that for? And of course, just like Mint, I can bring in all of my various accounts that I have. So it brings my credit card accounts together, my mortgage, my bank accounts, my investment accounts, pretty much anything I can include in there.

Reviewing your financial goals and managing your finances long term

And it even pulls in my credit score and my husband’s credit score, and we can collaborate within the app as well. So that’s been really cool to be able to use that as a married couple.

So if you all are interested in Monarch. I can do more content around this. Just let me know below if there’s interest here, and I can show you specifically how I use it. It has some really cool functionality and honestly, I think it’s going to change the game when it comes to my personal finances.

Now, like I said, it does come with a monthly subscription fee, but I’m gonna tell you it is well worth it. And of course, I can save you money on that too. So you can find out more about Monarch at jb troll.com/monarch.

And normally the fee for the full year is 99.99, which comes out to a little over $8 a month. But of course, if you use my code, you’re gonna be able to save 50% of that. So definitely use my code to save 50% off your full first year with Monarch.

Final thoughts on managing your finances and staying organized

And if you try it out, definitely make sure to comment down below and tell me how you feel about it. Personally, I’m loving it, but I wanna hear from you if you found it really helpful and what you like most about it.

So for me, 2025 was the year of just reorganizing everything in my financial life, and that’s even as a CPA and someone who generally stays on top of this stuff. You still need to refresh every now and again, and while I try not to get distracted by all the new different softwares coming out and I don’t switch often.

I do think sometimes when you know something isn’t working for you anymore, it’s time to go look for something that will, and for me, these new tools have fit the bill perfectly if you’re in the market for new business tools as well. Make sure to check out this video that walks through all of the various different business finance tools I switched last year.

And make sure to check out the links in the description below if you’re gonna sign up and try Crew or Monarch, definitely make sure to use those links in order to save some money. And of course, if you have questions about these tools, make sure to ask them down below in the comments as well. Thanks for joining me and I’ll see you next time.