How to accurately determine if S Corp tax savings will apply to you

One of the most common topics I’m asked about as a CPA relates to WHEN it makes sense to become an S Corp.

There is a lot of incorrect information out there on this topic, so I’m going to provide some tips and advice to keep in mind when deciding whether or not the S Corp route is the right one for you.

Furthermore, I’ll empower you to assess whether the service provider offering advice is giving accurate information.

Why many believe S corp tax status will save money

Let’s go over the potential tax savings of becoming an S Corp.

Before we do, I want to explain why there are advantages to an S-Corp tax status.

An LLC or sole proprietorship typically doesn’t receive the same tax savings as an S Corporation.

That said, there are some things you should consider when it comes to S Corp calculators and calculating your potential tax benefits.

If you’re an LLC or a sole proprietor, the income you make from your business is considered to be one amount (your profit) and is subject to both income and self-employment taxes.

Self-employment tax includes Social Security and Medicare and amount to 15.3% of your total profit up to the phase-out limits.

By becoming an S Corp, you may be able to reduce your taxes.

Instead of paying self-employment tax (which covers Social Security and Medicare) on the full amount of your business income, you would only have to pay that 15.3% on a portion of it.

This can result in a lower overall tax burden, but you’ll also have to factor in income tax brackets.

So what’s the difference if you’re taxed as an S Corp?

As an S Corp, you can separate your income into two distinct buckets, one of which is subject to both self-employment and income tax.

The other is only liable for federal and potentially state income taxes.

(Which is why this article’s breakdown of your potential S Corp distribution tax calculator is so valuable!)

This can help reduce your overall tax burden compared to the amount you’d pay as an LLC or sole proprietor.

Now, how do you do that?

You implement a s corp tax estimator that helps you compare all of the fees you might incur.

The role of reasonable salary, aka reasonable compensation

As a business owner, you can determine an appropriate amount for your salary, which will then be taxed according to the income tax brackets and will have self-employment taxes taken out.

Any income (i.e. profit) in your S-Corp beyond this salary, however, can reduce your total payroll taxes liability as it avoids self-employment taxes (though you still have income taxes on this portion).

When you pay yourself salary as an S Corp, all applicable taxes must be paid.

However, if you take out additional profit above and beyond your reasonable salary (known as owner’s draw) only income taxes are due – not self-employment tax.

This potentially saves you the 15.3% self-employment tax rate.

The OLD WAY to apply an S corporation tax calculator

Here’s an example.

Let’s say you have a profit of $100,000 before paying yourself. You determined a reasonable compensation amount for yourself from your business of $60,000 and estimated that the left over profit is $40,000. In this instance, it may seem simple to calculate a potential tax savings of 15.3% on the total $40,000 by multiplying it out for a total of $6,120.

This “back-of-the-envelope” method is employed by many accountants…but it isn’t accurate.

This calculation does not a tax savings make!

Here’s why there is more to a corp tax savings calculator

It is important to consider ALL factors when evaluating whether an S Corp or other business entity would be the better choice for you.

When making calculations, make sure to include any deductions, credits, and taxes that may be applicable. An accountant should be asking you about your full tax situation, including spousal income if you are married filing jointly, and any other income or deductions you may be eligible for.

If they aren’t asking you this when making an assessment of whether S Corp is right for you, you could find yourself with incorrect advice from an accountant or advisor on the subject.

Some accountants even use old-school “rules of thumb” to recommend S Corp, such as profit thresholds. While a profit of $60k+ might indicate an S Corp COULD save you money…just reaching that profit level does NOT mean that it will. A full calculation should be performed before taking any action.

It is important to ensure this information is taken into consideration as it can save you time and money in the long run.

S Corp Tax Deadlines Approaching Fast! Learn More ⬇️

Enter the QBI Deduction: The Qualified Business Income Deduction

When looking at taxes for different types of businesses, it is important to factor in the Qualified Business Income deduction.

This deduction was introduced in 2018 as part of the Tax Cuts and Jobs Act, and can have a significant effect on tax liabilities.

Be sure to include this when making your calculations.

The QBI deduction can be a difficult concept to grasp, and is a multiple course topic for accountants.

That being said, it is possible that the deduction may make an S-Corp less attractive due to the potential savings on self-employment taxes.

It is important to understand the QBI deduction and its potential impact on federal income tax, which can outweigh the positive impact an S election may have on self-employment tax.

Especially if you are an S-Corp where the full deduction may not be available.

Better questions to ask vs. an outdated corp tax calculator

To be able to estimate the QBI deduction impact, your service provider also should be asking you questions about the rest of your income, especially if you have additional sources of income.

It is essential to consider all sources of income and other deductions when assessing federal income tax.

This includes income from a partner or spouse if filing jointly, as well as any additional itemized deductions.

All these factors will have an impact on what your final federal income tax rate is.

Make sure you don’t let your accountant give advice based solely on how much money your business made.

The old rules don’t work anymore, so take a more detailed look to get the right tax advice.

When to take a look at S Corp tax status as a business owner

If you’re thinking of making a switch, take a closer look when your profits reach around $60,000-$70,000.

Don’t assume that automatically means an S Corp is the right way to go; make sure your compensation is reasonable if you do decide to become an S Corp.

Be cautious when deciding your salary as the IRS won’t hesitate to come after you if they suspect that you are attempting to avoid self-employment taxes.

Make sure the salary you set is reasonable and defensible.

You can use the tools in our S Corp Toolbox to estimate your reasonable salary for the purpose of the LLC vs. S Corp tax calculation.

However, if you want the most IRS defensible reasonable compensation support, we recommend getting the S Corp Toolbox Plus which comes with a personalized CPA-reviewed Reasonable Compensation Study and Report specifically for you (plus you’ll save $100 on the bundle!).

Self employment tax considerations and retirement planning

Now, another important thing you want to be considering when you are thinking about becoming an S Corp is what your planned retirement contributions are and what types of retirement accounts you plan to use.

The choice between S Corp or LLC can have a major impact on what you’re able to put into your retirement accounts and the amount of tax you ultimately owe.

Due to the complicated language, take a close look at the various options like SEP IRAs and solo 401ks.

When deciding between an S Corp or LLC and budgeting for taxes, consider compliance too.

On average, it costs S Corp owners at least $2k more in compliance costs (tax filings, payroll platform, etc) to be an S Corp vs. an LLC.

Additional compliances to consider when becoming an S corp

Look at all factors, not just the tax savings. How much money will actually end up your pocket in the long run?

Even if you would save money through an S Corp tax filing, don’t forget to factor in the extra paperwork and potential expense of additional tax filings.

Evaluate all costs beyond taxes, such as paperwork and payroll costs that come along with an S Corp filing.

You’ll also likely have more expensive bookkeeping to take into account too.

Not all accountants will mention this when they perform an S Corp analysis, in part because they have a vested interest in your conversion to S Corp status since they’ll be able to charge higher fees to help you elect S Corp and stay compliant.

A more cost-effective way to determine if S Corp is right for you would be to calculate your potential savings independently via our S Corp Toolbox.

It will educate you on how to stay compliant as an S Corp, help you perform a detailed calculation of tax savings (including the QBI deduction), help estimate reasonable compensation, show you how to make the election yourself for free, and provide a comprehensive picture of S Corp compliance.

For more information, go to JamieTrull.com/SCorpToolbox.

A practical reasonable salary example

Using the numbers from before, we will enter a $100,000 income (profit from your business) into a special tax calculator I use as an accountant.

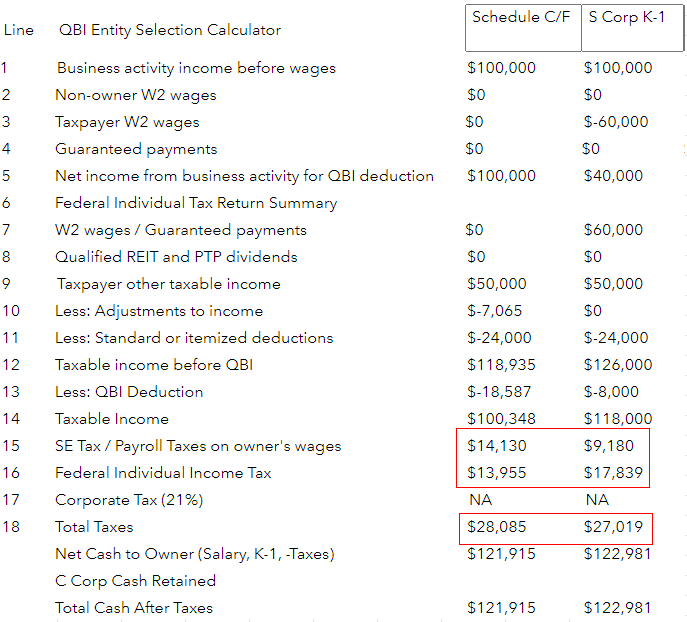

We will assume you will pay yourself $60,000 annually. This results in a total of $40,000 not subject to self-employment tax.

This scenario also assumes that your spouse has $50,000 in additional income, and that you take the standard deduction and make no contributions to a self-employed retirement plan.

Doing the back-of-the-envelope calculation employed by many financial professionals, we would calculate the savings as:

$40,000 in owners draws x 15.3% self-employment tax savings = $6,120 in tax savings as an S Corp. Many professionals would use this to recommend a change to S Corp status.

However, the actual results of a detailed S Corp calculator reveal that this methodology is not necessarily accurate:

When you look at total taxes (Line 18), an LLC will pay about $1,000 more in this scenario than an S Corp.

When we focus on self-employment tax specifically, the savings lands around $5,000. Not quite the $6,000 ish we thought it would be, using the back-of-the envelope method, but pretty close.

However, it is the increase in federal income tax due to the reduction of the Qualified Business Income Deduction (QBI) that flips the script.

In this scenario, our federal income taxes went up by nearly $4,000, almost entirely offsetting the self-employment tax savings.

Make sure to account for your own situation and ensure you factor the QBI deduction into the S Corp tax calculation.

What’s the moral of the story?

Avoid generalizations or rule of thumb when making a final decision.

Instead, consult a financial expert and make sure you have a thorough insight into all factors before making your decision.

When looking into an S Corp, get help from a trusted advisor (accountant or CPA) who takes all of these factors into consideration. .

Alternatively, you can use Jamie Trull’s S Corp vs. LLC Calculator and Selector available inside our ‘S Corp Toolbox’ to do it yourself and save on sometimes accountant fees.

Plus, get a fully independent assessment on what type of entity makes sense for you right now and in the future.

The ‘S Corp Toolbox‘ also provides helpful resources to estimate reasonable salary, make the election yourself for free, and stay compliant with the rules, all while saving the most you legally can on taxes.

We hope today’s blog provided value and informed you on important S Corp topics. Be sure to take advantage of the totally free S Corp success checklist available on our website.

If you’re looking for more detailed information, be sure to check out our YouTube video where I go into further detail about the S Corp topics discussed today.

Frequently Asked Questions About becoming an S Corp Owner

How much will I pay in taxes as an S Corp?

Taxes for S Corps can be a tricky subject.

Fortunately, this helpful blog post or the video above can help guide you through the process of understanding taxes for S Corps.

Are S corps taxed at 21 %?

No. The 21% rate applies to C Corporations not taxed as an S Corp. A specific S Corp rate does not exist. As a pass-through entity, your profits determine your taxes. Your personal tax rate depends on income, deductions, and credits.

While we don’t go into C Corps in detail on this blog post, note that C Corps differ in that they are subject to double taxation.

That means that while the Corporate rate is a low 21%, any amounts you take out of the business to pay yourself as the owner get taxed also.

For an S Corp, LLC, or Sole proprietor, you will pay taxes at the personal level (thus the pass-through designation as the income “passes through” to your personal tax return).

Which is better for taxes, an LLC or an S corp?

Deciding between an LLC and an S Corp depends on various factors.

This includes the amount of profit in your business, your other income and deductions. As well as your plans for retirement contributions and health care.

Generally speaking, S Corps can be advantageous for the right businesses when it comes to tax savings. Why?Because they offer lower self-employment taxes.

However, you also need to take the impact of the Qualified Business Income Deduction (QBI) into account.. Looking at payroll taxes alone is not sufficient.

It’s best to speak with a professional to understand your options.

Watching the video below will also help to educate yourself on the many moving parts of the decision.

Who pays more taxes, LLC or S corp?

In the past, it was a general rule of thumb that LLCs pay more taxes than S Corps.

S Corps can sometimes save money for business owners as a portion of their earnings can avoid self-employment taxes (social security and medicare).

LLCs conversely must pay self-employment taxes and income taxes on all of their earnings.

However, as discussed in this article, the Tax Cuts and Jobs Act created new guidelines and introduced the Qualified Business Income (QBI) deduction.

This made the calculations much more complex.

Consult a tax professional to determine which structure is best for your business.

Or, use the tools within our S Corp Toolbox to independently calculate your savings.