How Does S Corp Save Taxes? Can You Really Save Tax Dollars?

Have you been wondering how an SCorp Save Taxes? Or if it really can?

Hello. Hello everyone. Jamie Trull here, your favorite CPA and financial literacy coach.

And today we're going to be diving even deeper into the world of S corporations, also known as S Corp. So this is perfect for you.

If you're wondering if being an S Corp saves you money, that's what we're going to answer here today.

So if you're wondering:

- How do taxes for S Corp work?

- Am I really gonna save if I become an S Corp?

- Is it worth it to be an S Corp?

Those are all the questions that we're really going to be talking about. So I'm glad you're here.

Now, my guess is if you are watching this video or searching if an S Corp can Really Save you Money, it's because …

You're Trying To Decide If Being An S Corp Is Right For You

And if it would save you in taxes, so you're in the right place.

But before we even get into the tax piece of things, I want to talk about how to understand S Corp in general and what they are. When we talk about being an S Corp, I want to kind of separate for you the idea of a legal entity and a tax entity.

Is an S-Corp a legal entity?

An S Corp, in general, is a tax election. It's not a true legal entity. So even though we might typically say things like I'm an S Corp, right?

Actually, in reality, what you are is whatever type of entity you have from a legal perspective. Taxed as an S Corp, or that has elected to be taxed as an S Corp.

If we wanna get wordy with it, okay?

So if you are an LLC. You could be a single-member LLC or a multi-member, LLC and then elect to be taxed as an S Corp. The LLC is still your legal definition. It's still the legal entity that you are when it comes to everything in the legal world, okay?

What is an S Corp Election?

The S Corp election is only for federal taxes. That's really what it is talking about.

It's an election for how you are taxed. So in general, if you're an LLC electing S Corp tax treatment, you are still an LLC for legal purposes.

But you are treated and taxed as an S Corp for tax purposes, okay?

On the flip side, you can also be taxed as an S Corp if you are a C corporation and elect to be taxed as a S Corp, okay? So that's the legal entity, is the C corporation in this case.

And you can make that tax election to be taxed as an S corporation.

You're still a C corporation, you still have to keep up with all the things you would and all of the additional administrative things and requirements of a C corporation.

But you are taxed as an S corporation for federal tax purposes, but for legal purposes, you're still a C Corp.

What is a tax election?

So I hope that designation helps because I think that that's one of the most confusing things when we are talking about this topic, is that people think that it's a completely different entity type and it isn't. It is fully a tax election.

And to get that tax election, you are filing a specific form that's just like a two-page form where you can elect to be taxed as an S Corp. Whether you're an LLC or you're a C Corp. Now, most of the time the people who follow me on this channel, you probably are more in the camp of being an LLC, thinking about becoming an S Corp, or maybe you're a sole proprietor thinking about getting your LLC and then electing S Corp tax treatment.

Is this advice for C Corps?

I don't speak as much to the C Corp because that's just kind of a different deal over here. And if you are a C Corp, please, please, please have a CPA that you are working with routinely.

Because there are a lot, a lot, lot more that you need to be thinking about and planning for as a C corporation. But today, we're gonna be diving into what it means to elect to be taxed as an S Corp. If you are an LLC or plan to have one.

Now, as a real quick aside. Even though I don't get a ton into C corporations, if you have heard about corporations getting double taxed or double taxation on corporations, that is talking about C Corp. So if you're wondering, are S corporations double taxed? The answer is no. So that's a reason that some C corporations may choose to be taxed as an S Corp. Because it could prevent that double taxation.

How To Avoid Double Taxation

Now, it depends on your facts and circumstances whether that's gonna make sense for you. but I just wanted to mention that S corporations, very much like LLCs, okay, are pass-through entities. And what that means is they are not taxed separately at the corporate level. All of those taxes pass directly through to your personal tax return.

When you hear pass-through entity, it just means that you don't have double taxation. You're taxed one time and you're taxed personally. But your business income flows through to your personal tax return. If you are a C corporation, on the flip side, you're gonna be taxed at the corporate level. And then when you take distributions out of the company, you're gonna be taxed again at the personal level.

That's what it means by double taxation. Okay, so aside over. Let's talk about this concept of saving money on taxes as an S corporation and how that happens. Now, if you are an LLC for instance, you are paying a couple of different types of taxes on your profit in your business.

So that profit is passing through to your personal return.

Let's Talk Taxes: Self-Employment Tax and Payroll Taxes

But that profit, right, which is your revenue less, your expenses, whatever's left. It's getting taxed in a couple of different ways on that personal return. With income taxes, right? Federal income taxes.

And you are being taxed with payroll taxes or self-employment taxes. Essentially it's Social Security and Medicare. So that is the other side of the coin.

A lot of people don't realize that both of those taxes are combined. AND are included in the calculation on your personal tax return that you have to file by April 15th.

So that's just something to know, is that two pieces of the pie are factoring in there.

Income Tax vs. Payroll Taxes

And importantly, where income tax differs from payroll taxes, right, is that income tax is really when you think about the tax brackets that you're in, right? Where maybe the first X amount is not taxed at all. And then there's that graduated scale for your tax brackets that's talking about income tax.

So for a period of time, you're not subject to income tax, and there is an exclusion of in 2024, it's $13,850 for what you can make without having to pay any income tax. So it's a more graduated scale.

But when you think of traditional taxes, that's probably what you're thinking of. Usually that makes up the bulk of what you're paying. But as self-employed people, we have a decent amount more taxes that we are paying on the self-employment side because we have to pay both the employer and the employee portion of payroll taxes. Which then combined becomes self-employment taxes.

Self-Employment Taxes Add Up

So income taxes over here, self-employment taxes over here. Both of those are combined on your individual tax return. Now here's the thing about self-employment taxes: It ends up being a little over 15% when you add it together. Again, you're playing employee and employer or portion. So adding those together a little over 15% and it's off of the first dollar you make, there's no exemption for the first X amount of dollars.

It's not a graduated scale like it is with income taxes. Instead, it kicks in immediately. So if you are self-employed, even if you only made $5,000, that's why you have to file a tax return, okay? 'cause that $5,000, even though it maybe doesn't have any income taxes, if you didn't have any other income, right?

It still will have self-employment taxes that start from dollar one.

Sole Proprietorship vs. LLC vs S Corp?

So that's kind of the difference with self-employed. Now, that's the case. If you are a sole proprietor or maybe you have created an LL. That is how you're gonna be taxed every dollar of profit, right? You are gonna have self-employment taxes to be paid up until you make a couple hundred thousand dollars in profit. Then you cap out on social security.

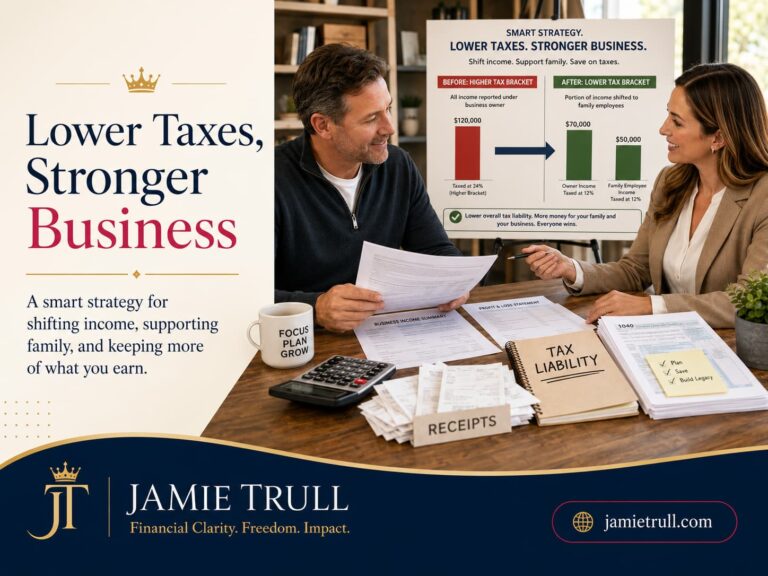

But in general, it starts from dollar one. So if you elect to be taxed as an S Corp, the benefit you get that you don't otherwise as any other pass-through entity? You get to separate your income basically into two different buckets. And one of those buckets? Taxed less than the other.

Where Does Profit Fit In When Choosing S Corp vs LLC?

What I'm talking about is when you have profit in your business, part of that is gonna get paid out to you as actual salary. Just like you or any other employee. Usually, you're gonna use payroll, you're gonna generate a W2, you're gonna withhold taxes, all the things, right? You're essentially paying yourself as an employee of your business that's gonna have all the same taxes associated with it, income taxes, and you're gonna have employer and employee side of payroll taxes, IE self-employment taxes.

So you're gonna pay all of that on that piece. That's considered your reasonable salary. But as an S Corp, you also get to pay a portion of your earnings more in distributions, let's say. You can call them dividends or distributions or draws, right? But ultimately, that's taking the excess profit that you have made in your business out of your business to pay yourself.

Or even if you leave it in your business, it doesn't matter. Again, because we're talking about a pass-through entity. So whether you keep it in your business or you take the profit out of your business, you're still gonna be taxed on it. But that piece above and beyond your reasonable salary does not have that second tax associated. So you're not going to have self-employment taxes on that piece.

You Are Still Going To Have Some Income Taxes

You have income taxes on pretty much every income you make from all different sources. But your self-employment tax does not apply. Now, you may be wondering why in the world can you do that. The income that you pay yourself as an employee is gonna be taxed just like any other income that's gonna have all the taxes.

And it's gonna have those payroll taxes on it because you're paying yourself. Essentially, your payroll for working in the business. The portion that is related more to you being the owner and investor of the business. Not actively working in the business, but kind of investing in the business.

Taking on the risk of investing in the business. That portion is not gonna have payroll taxes associated with it because it is not compensation for working in your business.

Payroll vs. Owner/Investor Compensation

It's compensation as an owner-investor, okay? So that's why you're only gonna have income taxes and not payroll taxes on that point. Now, I could go on a whole diatribe here. I will be honest about how a little bit crazy it is. The fact that the income that we work for is taxed more than the income that we don't. Which seems a little bit backward, if I'm being completely honest. But that's not what this video is about. Maybe I'll make another one later that goes more into my thoughts on that.

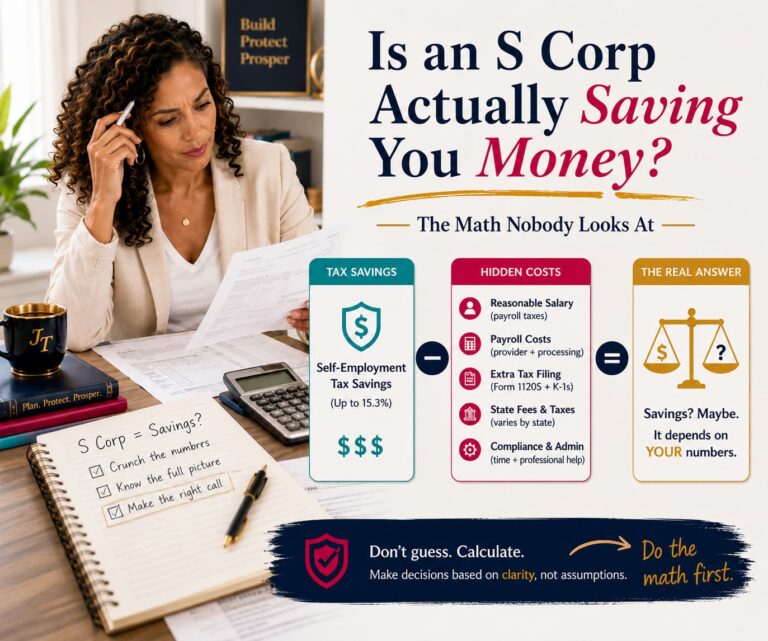

Corp Tax Calculator and Common Misconceptions

So now I'm gonna do a little bit of a calculation. And we're gonna talk about some common misconceptions and some things your CPA may not be telling you when it comes to S Corp, because you may have heard this and you might be thinking, wait a second, hang on, this sounds great.

Why wouldn't somebody be an S corporation if it allows you to lower taxes on a portion of the income you make in your business? Right? Why wouldn't you do that? Well, it does not make sense for everyone. And there are a lot of CPAs, a lot of accountants out there who still do a little bit of a back-of-the-envelope calculation when it comes to determining if this is right for you.

And they might even use rules of thumb that are very, very outdated. So be careful anytime you hear a general rule of thumb because things changed for S corporations back in 2018 which made this calculation much more complex. It also means that somebody can't tell you if an S corporation is right for you without gathering a large amount of information about your personal tax situation from you.

Beware blanket advice regarding corporation tax status

So just be careful of any blanket advice you're getting from a stranger on the internet from your brother's friend or even from your CPA. Just make sure to triple-check and make sure they're including all of the different factors. Not just federal taxes when they are recommending this to you. 'cause there are more things to consider, and I'm gonna get to that in a minute.

But let's do a quick calculation just because I think that that can be helpful to be able to see this in real-time. So let's say, I'm gonna use my little trustee calculator. Let's say that your business profited, before paying yourself anything, a hundred thousand dollars, okay? And then let's say you spent some time to figure out that your reasonable salary is $60,000.

Reasonable Salary Compensation

Again, don't use a rule of thumb here. You want to do something more formal and documented as to how you came up with that. I have tools that can help that. That's not the purpose of this video. But I do have tools where you can do a reasonable compensation study if you're trying to figure this out.

But for the sake of this example, let's say you decided $60,000 was a reasonable salary for the work that you did in your business. So that means $40,000 is your profit in excess of your reasonable salary. So $40,000 times, the roughly 15% that we're gonna save on that portion is $6,000. You might be looking at that and being like, yeah, I'd like to save $6,000 in taxes. Why would I not do that?

Enter the Qualified Business Income Deduction

Well, that's not super accurate. Because again, some new changes were made back in 2018. Which I guess isn't that new anymore. but those changes made it a lot more complicated.

It's called the QBI deduction. Or the Qualified Business Income deduction. And it gets a little crazy, and I am not gonna get into that here. There are hours of workshops that CPAs can watch on this if you're interested.

That's not what I'm gonna be doing on YouTube today. But suffice it to say, right, we did all of that and we still came out with this $6,000 in savings. Should we do this? Are we gonna save $6,000? Here are a few things to keep in mind. Let's say we validated and yes, we're gonna save $6,000 in federal income taxes.

Additional Fees For Filing As An S Corp

Here are the other things to consider. Number one, how much additional administrative costs are you going to have by being an S corporation? You're gonna have an extra tax filing. You have an 1120-s that's due March 15th every year. It has its tax filing for an S Corp. So that's something to be aware of.

You're gonna have to run payroll, and if you don't currently run payroll for any employees, that's gonna be an added service you're gonna have to pay for yourself to run payroll and be compliant with payroll. You're probably gonna end up spending more money with your CPA to help you with some of these requirements. To make sure a reasonable salary is correct, to keep everything documented, to track your balance sheet, and your basis in a non-corporation, right?

It really, your balance sheet isn't as important. You don't have to report on that for taxes. You only really give your profit and loss, so your income and expenses. But when you are in S Corp, you have additional things that you have to report and you have to track. And that means you're gonna maybe need upgraded software or maybe need to pay your CPA more, right?

Track What You Need For Tax Season

To be able to make sure you're tracking what you need to for tax purposes as an S corporation. So all of that can add up to a few thousand dollars pretty quickly, and it can vary depending on how complex your business is, and exactly how much it ends up being, but that's just something to be aware of.

And the other thing, other than administrative costs, you also need to make sure that you understand the rules and the requirements for an S corporation in your state. Because certain states may tax an S corporation more than such as an LLC would be taxed. And that is because they have things like franchise and excise taxes, additional business taxes that are going to say, okay, if you didn't pay payroll taxes on that piece, we are gonna tax it at the state level.

And Tennessee, the state that I live in, happens to be one of those states right now that does have a franchise and excise. That does limit quite a bit the benefit I get from being an S Corp. I did finally become an S Corp, but it was a lot past the dollar amount in profit that is. The typical rule of thumb would tell me would be the time to switch when I did the detailed calculations, it was quite a bit past that before it made sense for me. Now, if you're wondering what are the rules in my state, you're gonna have to go to your State Department of Revenue and dig into it and see it can be a little bit difficult to find.

Looking For The States With The Best Tax Savings?

I will say that there are four states where it can have the biggest impact and offset a lot of those federal tax savings. And those states just happen to be Louisiana, New Hampshire, New Jersey, and my home state of Tennessee. That doesn't mean that there aren't taxes in other states, they do exist. But those are the four that I know tend to have taxes that will very much create a situation where there is a longer road before it makes sense for you to be an S Corp.

It still may make sense for you at some point, but perhaps not right away. So if you're wondering what you should do, what's the conclusion here? How do I know if I should become an S corporation? Well, you can of course start with your CPA or accountant, but again, sometimes they're not gonna necessarily fully give you the entire picture.

And that may be because maybe they're not knowledgeable about it or up to date on the rules. But it also can be because honestly, they often will be the benefactor. If you are an S corporation, some of those fees for payroll and for those extra tax returns are gonna go to your accountant. So they may have a little bit of an incentive to tell you S Corp is right for you, which is why I highly, recommend empowering yourself. Do the calculation yourself if you can.

Find The Best Corp Tax Savings Calculator For Your Business

There are tools that I have that can help you do that and get a completely unbiased opinion on whether S Corp is right for you and also help you make the election yourself if you decide that it is right for you.

It's also gonna walk you through things like making sure that you don't have an unreasonable salary and ensuring that you are staying compliant with all the rules and regulations of being an S Corp. So if that sounds good to you, definitely go check out https://jamietrull.com/scorptoolbox.

You are going to be able to find all the different resources in there to learn more about S Corp, figure out if they're right for you, and have all the tools to stay compliant with the IS guidelines.

And I also have other content that you can dive into here on YouTube that talks even more about S, Corp, things like reasonable salary, all the things you wanna know to set yourself up for success and not miss out on any potential tax savings.