Your cash flow vs profit scenario: your P&L says you’re profitable… but your bank account says “yikes.”

If that sounds familiar, you’re bumping into one of the most misunderstood truths in business: profit and cash flow are not the same thing.

Understanding the difference (and managing both) is the line between constant money stress and steady, sustainable growth.

Below, you’ll get a plain-English breakdown of profit vs. cash flow, the top reasons they diverge, and a practical system to fix the gap, including simple tools and automations you can set up in an afternoon.

This post is sponsored by Freshbooks. All opinions expressed are my own.

Profit vs. Cash Flow (and why both matter)

Profit (on your Profit & Loss statement) is a formula:

Revenue – Deductible Expenses = Profit (Net Income)

It’s driven by accounting rules. That means it includes things that don’t always move cash (like depreciation) and may recognize income/expenses at different times than the cash actually moves.

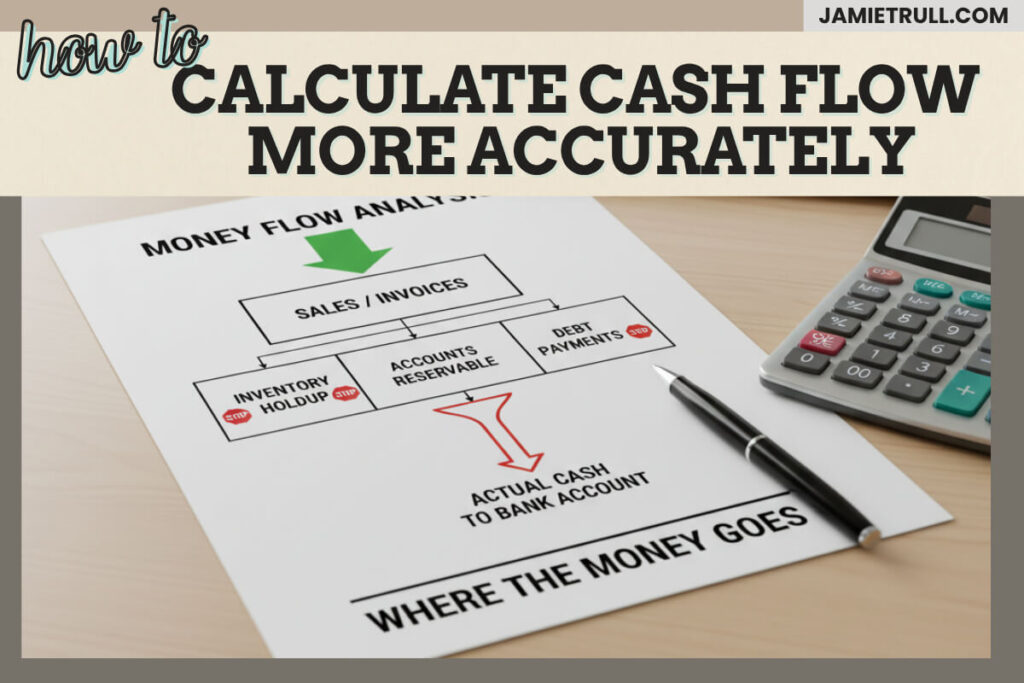

Cash flow, on the other hand, is what hits your bank. It measures real dollars in and out—the money you can actually spend to make payroll, pay vendors, and invest.

You need profit to prove your business model works.

You need cash flow to keep the lights on.

The accounting lens that confuses everything (accrual vs. cash basis)

- Cash basis recognizes income when you receive it and expenses when you pay them. Simple. Great for many small businesses.

- Accrual basis recognizes income when you earn it (even if unpaid) and expenses when you incur them (even if unpaid). Better decision data… but the timing differences can make profit and cash flow look out of sync.

If your bookkeeper runs accrual books (or you’re required to for inventory), your P&L can show profit before the cash arrives—or show an expense before you actually pay for it. That’s how you can “make money” on paper and still be short on cash.

9 common reasons profit ≠ cash (with fixes)

1) Accounts Receivable (invoices you haven’t collected yet)

- What happens: You record revenue on your P&L when the work is done, but the customer hasn’t paid yet. Profit up, cash not yet in.

- Fixes:

- Require deposits or milestone billing.

- Offer ACH/autopay.

- Add net terms aligned with your cash needs (e.g., Net 7 or Net 15 instead of Net 30/45).

- Set automated invoice reminders and late fees.

- Require deposits or milestone billing.

Metric to watch: DSO (Days Sales Outstanding). Lower is better.

2) Accounts Payable (bills you owe but haven’t paid)

- What happens (accrual): Expense hits your P&L but cash hasn’t left yet. Profit down, cash unchanged (for now).

- Fixes:

- Batch pay bills on a schedule.

- Negotiate vendor terms (Net 30 → Net 45) to align with when you collect.

- Batch pay bills on a schedule.

Metric to watch: DPO (Days Payable Outstanding). Higher (within reason) improves cash.

3) Inventory (cash leaves now, cost hits later)

- What happens: You spend cash to stock up. On the P&L, that purchase doesn’t hit expense until the item sells (as COGS). Cash down today, profit unaffected (yet).

- Fixes:

- Set reorder points and open-to-buy budgets.

- Trim slow SKUs, increase turns, and right-size orders.

- Protect a dedicated inventory budget so you’re not starving payroll/taxes.

- Set reorder points and open-to-buy budgets.

Metric to watch: DIO (Days Inventory Outstanding). Lower is better.

4) Debt payments (principal doesn’t hit the P&L)

- What happens: Monthly loan payments include interest + principal. Only interest is an expense. Principal reduces the loan balance on your balance sheet (not your P&L). Cash down, profit only slightly down.

- Fixes:

- Forecast principal outlays in your cash plan.

- Refinance high-rate debt where appropriate.

- Forecast principal outlays in your cash plan.

5) Capital expenditures (equipment) & depreciation

- What happens: You buy equipment today (big cash out). On the P&L, you expense it slowly over time (depreciation).

- Fixes:

- Budget CAPEX and plan purchases around your cash cycles.

- Discuss accelerated depreciation options with your CPA at tax time.

- Budget CAPEX and plan purchases around your cash cycles.

6) Owner draws / distributions

- What happens: Money you pay yourself as an owner draw/distribution is not a P&L expense. It reduces cash, not profit.

- Fixes:

- Pay yourself from a dedicated Owner Pay bucket (see envelopes below).

- Put owner comp in your cash forecast, not your P&L.

- Pay yourself from a dedicated Owner Pay bucket (see envelopes below).

7) Taxes & quarterly estimates

- What happens: P&L doesn’t accrue exact taxes due. When you send quarterly estimates or a big April payment, cash drops fast.

- Fixes:

- Auto-sweep a percent of deposits into a Taxes account.

- Forecast quarterly outflows so nothing surprises you.

- Auto-sweep a percent of deposits into a Taxes account.

8) Payment processor holds, chargebacks & timing

- What happens: Merchants delay deposits, batch funds, or hold reserves. Cash hits later than expected.

- Fixes:

- Check funding schedules and adjust your forecast.

- Keep an operating buffer to absorb timing hiccups.

- Check funding schedules and adjust your forecast.

9) Prepaid expenses & deferred revenue

- What happens:

- Prepaids: You pay insurance or software upfront. Cash leaves now; P&L recognizes expense over time.

- Deferred revenue: You collect cash up front for work performed later. Cash up, profit recognized later.

- Prepaids: You pay insurance or software upfront. Cash leaves now; P&L recognizes expense over time.

- Fixes:

- Spread big prepaids across your cash plan.

- If you take prepayments, remember they’re not “free money”—you’ll still need cash to deliver.

- Spread big prepaids across your cash plan.

Your Cash-Flow-First Playbook

Step 1: Build a rolling 13-week cash forecast

You don’t need fancy software. A clear spreadsheet beats an inaccurate app every time. Map starting cash, then add weekly expected inflows (customer payments, funding, other income) and outflows (payroll, rent, inventory, debt, owner pay, taxes, software, etc.).

- Update it every week (I do it on “Money Monday”).

- Look ahead 13 weeks—long enough to see problems and fix them.

Grab my ready-to-use template:

➡️ Cash Flow Template (plug-and-play): https://jamietrull.com/cashflow

Step 2: Separate your cash into “purpose” buckets (envelope banking for business)

One bank balance is a trap. It’s too easy to overspend and accidentally use tax money for an ad campaign. Use multiple checking/savings sub-accounts and automated rules so your money goes where it needs to—before you can “borrow” from it.

Common buckets to consider:

- Operating Expenses (bills, software, rent)

- Owner Pay (your paycheck)

- Taxes (quarterlies & year-end)

- Opportunity Fund (growth projects, courses, first 1–3 months of a new hire)

- Emergency/Buffer (2–3 months of core expenses)

- (Optional) Profit/Impact/Fun (stay motivated and mission-aligned)

Set up rules (e.g., of every deposit, move X% to Taxes, Y% to Owner Pay, etc.). Start simple, customize over time.

Tool that makes this easy:

➡️ Relay lets you open multiple business accounts, set automations, and manage cash like envelopes—all with modern, small-business-friendly banking.

Get $50 when you’re approved and fund your account with my partner link:

https://jamietrull.com/relay

(Relay is a financial technology company, not a bank. Banking services provided by Thread Bank, Member FDIC.)

Step 3: Tune your pricing & margins (so cash flow has room to breathe)

If you constantly feel like you “can’t afford to hire” or “can’t pay yourself,” it’s often a pricing problem.

- Price to cover: direct costs + your time at market value + overhead + profit.

- Track contribution margin (price – variable costs) by offer/SKU.

- Service businesses: include the market value of your labor even if you currently do the work yourself.

- Product businesses: fight margin erosion (shipping, packaging, returns, fees).

Small price changes + tighter scope = big cash gains.

Step 4: Speed up cash in

- Deposit upfront (20–50%) or milestone billing.

- Autopay ACH/CC for recurring services.

- Incentivize early pay (e.g., 1–2% discount) if it supports your cash cycle.

- Send invoices immediately (not “Friday when I have time”).

- Use consistent follow-ups and clear terms.

Step 5: Slow cash out (without starving growth)

- Ask vendors for Net 30/45.

- Batch payments (e.g., payables twice a month).

- Align big spends (inventory, CAPEX) with your forecasted peaks.

- Keep a hard floor in Operating so you don’t dip below your buffer.

Step 6: Protect the cushion

Decide your Minimum Operating Cash (MOC)—often 6–12 weeks of core OPEX for small businesses. Hold your MOC in a separate savings bucket so it doesn’t masquerade as spendable cash.

Relay’s dedicated accounts + savings make this simple.

➡️ Open your Relay setup: https://jamietrull.com/relay

Read your three statements together (not in isolation)

- P&L (Profit & Loss): “Am I profitable?”

- Balance Sheet: “What do I own/owe? What’s tied up in AR, inventory, debt?”

- Cash Flow Statement: “Where did cash come from/go?” (Operating, Investing, Financing)

Looking at all three is how you catch “growing broke” (e.g., solid profit, but cash is trapped in AR/inventory and debt is rising).

Common cash-flow traps (and quick fixes)

The Inventory Hamster Wheel

Trap: All profit reinvested into stock; no cash to pay yourself.

Fix: Set an inventory budget & reorder rules; skim a percent of sales to Owner Pay and Taxes every deposit.

Tax Time Panic

Trap: Paying taxes from Operating because there’s no tax fund.

Fix: Auto-sweep % of deposits to Taxes weekly. Forecast quarterly payments in your 13-week plan.

“Profit means we can spend!”

Trap: Celebrating profit without cash reality.

Fix: Make spending decisions using your cash forecast and envelopes, not just your P&L.

Ignoring your time in pricing

Trap: “I’m free” on the cost sheet → no room to hire or rest.

Fix: Include market-rate labor in your pricing. Owners aren’t free.

One big bank account

Trap: Money is fungible, so it gets spent on the loudest need.

Fix: Purpose-built accounts + automations (Owner Pay, Taxes, Buffer, Opportunity).

Metrics that keep you honest

- Operating Cash Flow (from the Cash Flow Statement): positive and growing.

- Cash Conversion Cycle (CCC): DSO + DIO – DPO. Shorter = stronger.

- Quick Ratio ((Cash + AR) / Current Liabilities): Aim > 1.0.

- Runway: Cash ÷ Monthly Core OPEX (in months). Aim for 2–3+ months.

Implementation checklist (do this this week)

☐ Download the 13-week cash flow template and load your next 90 days. https://jamietrull.com/cashflow

☐ Open dedicated bank buckets (Operating, Owner Pay, Taxes, Opportunity, Buffer) and set auto-allocations per deposit. https://jamietrull.com/relay

☐ Tighten invoicing rules (deposits, autopay, reminders, clear terms).

☐ Review pricing on your top 3 offers/SKUs for margin and labor coverage.

☐ Set your Minimum Operating Cash and move the cushion to savings.

☐ Put “Money Monday” on your calendar—update the forecast weekly.

Want a deeper dive into finding (and keeping) more profit?

My new book Hidden Profit shows you how to uncover money that’s already hiding in your business—then channel it into your goals using simple systems (like the cash-flow playbook above). It’s practical, owner-friendly, and built for real-life businesses.

➡️ Pre-order Hidden Profit: https://jamietrull.com/hiddenprofit

(Pre-order bonuses are available for a limited time!)

Final word

Profit tells you your business model works. Cash flow keeps your business alive. When you separate your cash into purpose-built buckets, forecast the next 13 weeks, and align pricing/terms to your cash cycle, the daily stress drops—and smart decisions get easy.

You’ve got this. Take 30 minutes today to set up the system that will pay you back all year.

Educational only; not financial, tax, or legal advice. Always consult your professional advisor for guidance specific to your situation.

Transcript: This transcript was generated from the video for your convenience, but it may contain typos or slight errors due to the transcription process. For the most accurate and complete information, we recommend watching the full YouTube video.

Understanding the Difference Between Cash Flow and Profit (difference between cash flow)

Your profit and loss is showing a profit, but your bank account tells a different story. Sound familiar? That’s because profit and cash flow are not the same thing, and it’s critical to understand the difference so that you can make. Better business decisions.

Today, I’m breaking down one of the most misunderstood concepts in business finances, and that’s the difference between profit and cashflow and why it matters more than you might think.

Hey everyone, I’m Jamie Trull, CPA Profit Strategist, and soon to be published, author of my very first book, hidden Profit, available for pre-order now. If you’re ready to stop leaving money on the table, hit that subscribe button and let’s get started and stick around to the end.

‘Cause I’m gonna talk about one of the most common traps that small business owners fall into when it comes to cash flow and a simple shift that can save you from financial stress.

Understanding Profit First

So first of all, what is profit?

Well, from an accounting perspective, profit is the difference between the money that you bring in and the money that goes out. So first. Let’s start with what actually is profit. And there are lots of different subcategories of profit, gross profit, operating profit, net income.

There’s a million different ways to slice it, but at the end of the day, profit itself is really just a formula. It’s revenue. IE, the money you made. Minus deductible expenses, which is the money that you spent that you can deduct for.

Taxes equals profit, and profit is what we pay taxes off of, but just to make things more complicated.

Profit has a thing that I like to call accounting funny business, and that’s what makes it more of a paper calculation than an actual in the bank thing. Now, typically you will see profit and cash flow align a lot of times, but not always. Because cash flow is what’s actually happening in your bank account.

It’s gonna track the real money that’s moving in and out, and it’s gonna exclude all that weird accounting, funny business. So you could technically have a profitable month on paper and still not be able to pay your bills, and that’s why cashflow and not profit is what actually keeps your business alive.

How Accounting Methods Affect Cash Flow (financial analysis)

So let’s talk about some of those different reasons that your cashflow might not align with your actual profit on paper. Now, the first and probably most common reason is if you are using the accrual basis of accounting.

Now, most of the time this is reserved for larger businesses, but ultimately that just means that you’re gonna record that income on your profit and loss as income when you earn it, not when you actually receive it.

So for instance, if you’ve earned income and you’ve invoiced the customer for that income that you’ve already earned, even if that invoice hasn’t actually been paid yet.

You can record that as income on your p and l, and similarly, if you’ve incurred expenses that you haven’t paid yet, they’re still accounts payable to you.

Those are included as expenses on your p and l upfront as well, even before you pay them. Now again, most smaller businesses.

Are cash basis mostly because it’s easier, it’s easier to track, and that means that you’re recording the income as income.

When you receive it, you’re recording the payments as payments when you actually make them IE when it’s leaving your bank account or when you charge your credit card.

Reasons Cash Flow and Profit Aren’t The Same

So that’s a really big differential for why cashflow might not equal profit if you are using that accrual basis of accounting.

Now, ultimately that just ends up being a timing difference, right?

Because maybe you’re recording that income and you’re not collecting it until later, but it can create what’s called a cashflow crunch.

So that’s happening to you and you’re profitable on paper. But your accrual basis, and you’re realizing that you don’t have any cash available, you might wanna look at how you collect cash.

So for instance, can you increase how quickly you collect that cash from customers?

Can you even bill upfront? In some industries, that’s totally acceptable to bill for work before you do it, and maybe even preferred because now you’re less likely to be chasing. Uncollectible accounts.

Inventory and Cash Flow Problems (cash flow problems)

But if you’re a cash basis taxpayer, that doesn’t mean that you are immune to having these profit versus cash flow differences. So we’re gonna talk about a few reasons that might still be happening to you.

Now, this is super common in inventory businesses. So if you’re a business that buys holds and sells inventory, then typically that inventory is not gonna be recorded as an expense when you pay for it.

So the cash is gonna go out the door, but you’re usually going to actually put that on your balance sheet.

And the reason for that is because of, again, accounting funny business. It’s one of the accounting rules that you can’t record it on the p and l as an expense until it’s actually sold IE cost of goods sold.

So that allows the revenue that you’re making, the money, the income that you’re making from the sale to align with when you’re recognizing that expense as well.

And that’s called what’s called the matching principle in accounting. Don’t worry, I’m not gonna get too deep into this, but ultimately the goal of the matching principle is for revenue and expenses related to a particular transaction to generally align as far as timing goes.

So if you’re buying inventory.

The cash is going out the door, but you’re holding onto it and not selling it for a while, right? Then you end up in a situation where you haven’t gathered the cash, you haven’t sold it.

So you haven’t collected the cash yet related to that inventory, and it’s just sitting on your balance sheet.

Balance Sheet Impacts on Cash Flow (balance sheet)

So the money’s gone out the door and you haven’t collected, you haven’t sold it, so you can’t actually expense it.

So now your profit, you might be showing that you’re profitable because those expenses aren’t showing up yet, but you don’t have any money in the bank, and this is really common.

Especially in Inventory businesses that are growing a lot because what you end up seeing is you end up taking the money that you make from your sales. And then you are reinvesting them back into more inventory and therefore you’re always in a situation wondering where the cash went.

It’s why I recommend anybody with an inventory business. Make sure to have an inventory budget and make sure you’re also routinely paying yourself.

It’s very easy to plow everything back into buying more inventory, and then it could be, you know, a long time from now before you actually get to see the fruits of that labor.

So take a little bit of profit along the way, even if you’re trying to grow your business quickly.

So inventory is one reason. Another reason your profit might not match your cash flow is if you’re making payments on debt. So I’m not talking about credit cards here necessarily. I’m talking more about longer term debt that you have, that you have interest payments.

Maybe you’ve got a loan that you took out for your business, right? And you’re paying off that loan. Well, that cash payment is actually going to be obviously reducing your cash flow ’cause it’s cash going out the door, but it’s not gonna be reducing your profit in your business.

Cash Flow or Profit? Understanding Debt & Depreciation (cash flow or profit)

And that’s because kind of like inventory, the debt that you entered into is actually on your balance sheet this time as a liability. And as you pay that off, that is what is going to reduce that liability.

So again, when you took out the debt, you didn’t have revenue that you had to pay taxes on for that debt, right? That was a good thing.

But similarly, now, as you pay off the principal amount, you’re not gonna have an expense for that debt either.

The only expense that shows up on your profit and loss is going to be the expense for interest that you’re paying on that debt above and beyond the principal payments.

So that’s another thing that can cause this mismatch of profit versus cash flow. You might be saying, well, wait a second, my accountant said I’m profitable.

But if all that money was going out the door to repay loans, you may not have any cash sitting in your bank account at the end of the day.

Now, another reason that you might end up in this boat of your cash flow and your profit being a mismatch is if you are buying assets for your business. Larger assets, machinery and equipment, things like that.

Those things are going on your balance sheet, right?

They’re not actually being expensed right away, typically. Now there are some different tax laws where you might be able to expense them more upfront, but if you’re in a situation where you’re not doing that, then you are likely going to be what’s called capitalizing them on your balance sheet.

Using a Cash Flow Statement to See the Full Picture (cash flow statement)

And what happens then is over time, over the useful life of whatever you bought, the uh IRS has all kinds of different useful life tables that you can figure out.

But let’s say it’s five years, you buy a new big computer setup. And it costs you $8,000, and so you’re actually recording that over a five year period. So you’re taking $8,000 divided by five.

I don’t know why I chose one. That wasn’t an easy thing to do in my head. Okay. I used my trusty calculator. It’s $1,600 a year if you’re depreciating it. You know, straight line.

So that means that you’re depreciating, let’s say $1,600 a year. That means that $1,600 a year of that equipment is what’s showing up on your p and l as an expense.

So instead of the full 8,000 that you paid upfront for this, you are instead getting a $1,600 deduction every year for five years.

So that’s another reason why your cash is not necessarily going to match up. With what you’re seeing on your p and l.

So again, you might have guessed that depreciation is another one of those things that I consider to be accounting funny business, and it just makes things much more difficult.

But again, the purpose is to match, right? Because you’re gonna use that asset not just in the first year. They don’t really want you, accounting rules, don’t want you to expense the entire thing.

They want you to match it with.

The time period in which they expect you to use that to generate income.

Cash Flow and Profit: Owners Draws, Tools & Planning (cash flow and profit)

So again, this is trying to match expenses and income, but it’s just making things a lot more difficult, especially for smaller business owners on the plus side.

That’s why the IRS does have some relief related to things like upfront depreciation that you can take accelerated depreciation.

So if you’re somebody who buys a lot of assets, you definitely wanna talk to your accountant about that.

And another reason that there might be a mismatch between profit and cash flow is if you’re taking distributions out of your business.

So if you are taking owner draws from your business, that is a balance sheet type of activity. It doesn’t show up as an expense on your p and l.

So that means that your p and l is gonna show as profitable, but you’ve already taken distributions of that cash out of your business and therefore reduced your cash balance.

Profit Does Not Equal Spendable Cash

So all that said, what is the biggest cashflow trap I see?

And it’s basically assuming that what your profit is is spendable cash, and unfortunately that’s just not the case. We don’t wanna make decisions based on profit alone.

It is important, but we also need to be considering cash flow.

So how exactly do we make sure that we’re maximizing our cash flow?

Well, first and foremost, it’s about the tools that you are using. So I have a few tools I use in my business. To help me with cashflow. Now, I actually don’t use a cashflow forecasting tool.

Mostly because I find them inaccurate and they can be really expensive. Instead, I have my own template that I’ve put together that I use literally every single week.

It is one of the things I do every, what I call Money Monday, I update my cashflow spreadsheet and I take a look to make sure I don’t have any ex. Expected shortfalls coming up in the weeks ahead.

So that has been a game changer in my business. It’s the best thing that I do every single week for managing my cashflow, and I actually made it available to you as well.

So you can go down below and check out my cashflow template or go to jamietrull.com/cashflow and you can grab it for your.

Other Tips To Manage Your Cash Flow

Now, the other thing that I do to manage my cash flow and use the systems that I have to help me is I use Relay, which is my business banking platform, to be able to separate my money into multiple different buckets for different purposes.

So if you follow this channel.

I talk a lot about profit planning. You can actually see a little bit more about profit planning and how I use Relay for my profit planning. In this video, however, I have to say it has been a massive game changer for me.

I’m ultimately able to separate my money into buckets for things like taxes and paying myself and reinvesting back into my business, even having some fun and also for making an impact. And doing things to help causes that you care about.

So you can do all of that with your profit, and it really helps to manage it in that way. And I love Relay because it basically allows me to use the envelope form of budgeting for my business so that I don’t accidentally steal from one thing to be able to pay for another.

So if you wanna check out more about Relay and also earn a $50 cash bonus once you fund your new account, go to jamietrull.com/. Relay to find out more and sign up.

What Negative Cash Flow Means: Find Your Hidden Profit

Now if you wanna go deeper into understanding this accounting funny business, or just understanding cash flow versus profit in a way that absolutely makes sense for a small business like you. I would love if you would pre-order my new book, hidden Profit that is coming out in October of 2025.

I’ve worked so hard on this book to come up with strategies to help you find profit that is already sitting within your business and to improve on things like. Cashflow and how you use your money to create the life that you want.

So please go to jamietrull.com/hiddenprofit and place your pre-order. It also means the absolute world to a debut author to have your support in the pre-order process.

And I have some extra bonuses for you too. So we’re offering over $300 worth of bonuses just for pre-ordering the book right now.

So make sure you go ahead and do that. Please literally go there right now.

Press this button on the screen, go pre-order hidden profit and claim your bonuses.

I’ll see you guys next time. Thanks so much.

FAQ: Understanding Profit vs. Cash Flow

1. What’s the difference between cash flow and profit?

Profit is what’s left over after your business subtracts deductible expenses from revenue. Cash flow is the actual movement of money in and out of your bank account. You can show a profit on paper and still not have enough cash to pay your bills.

2. Why does my profit look good, but my bank balance is low?

This often happens because of timing differences, inventory purchases, debt payments, or owner draws. Your profit includes accounting adjustments, while your cash flow reflects real money movement. A cash flow statement can help you understand where cash is actually going.

3. How do inventory purchases affect cash flow?

When you buy inventory, the cash leaves your account immediately, but the expense doesn’t hit your profit and loss statement until the inventory is sold. This can create cash flow problems, especially in fast-growing product-based businesses.

4. Are debt payments considered expenses?

Only the interest portion shows up as an expense on your profit and loss. The principal payments reduce your loan balance on the balance sheet, not your profit. This is another major reason profit and cash flow don’t match.

5. How can I calculate cash flow more accurately?

Start by tracking incoming cash (payments received) and outgoing cash (bills paid, debt payments, inventory purchases, owner draws). A simple weekly cash flow spreadsheet is often more accurate than forecasting software for small businesses.

6. Is cash flow or profit more important?

Both matter, but cash flow is what keeps your business alive day-to-day. You can survive a long time without strong profit, but not without positive cash flow.

7. What is a cash flow statement, and do I need one?

A cash flow statement shows how cash moves through your business across operating, investing, and financing activities. While many small business owners ignore it, it’s one of the best tools for understanding where your money actually goes.

8. Why doesn’t my accountant warn me about cash flow issues?

Because accountants primarily report on profit, not cash. Cash flow management often requires a separate system, like weekly cash tracking or multiple bank accounts for budgeting.

9. How can I manage cash flow better without expensive software?

Use a simple weekly cash flow template and separate your money into labeled accounts (taxes, owner pay, operating expenses, etc.). This helps prevent overspending and reduces financial stress.

10. How do owner draws affect cash flow and profit?

Owner draws reduce your cash balance but do not reduce your profit. This is one of the biggest misunderstandings for small business owners and a common source of confusion.