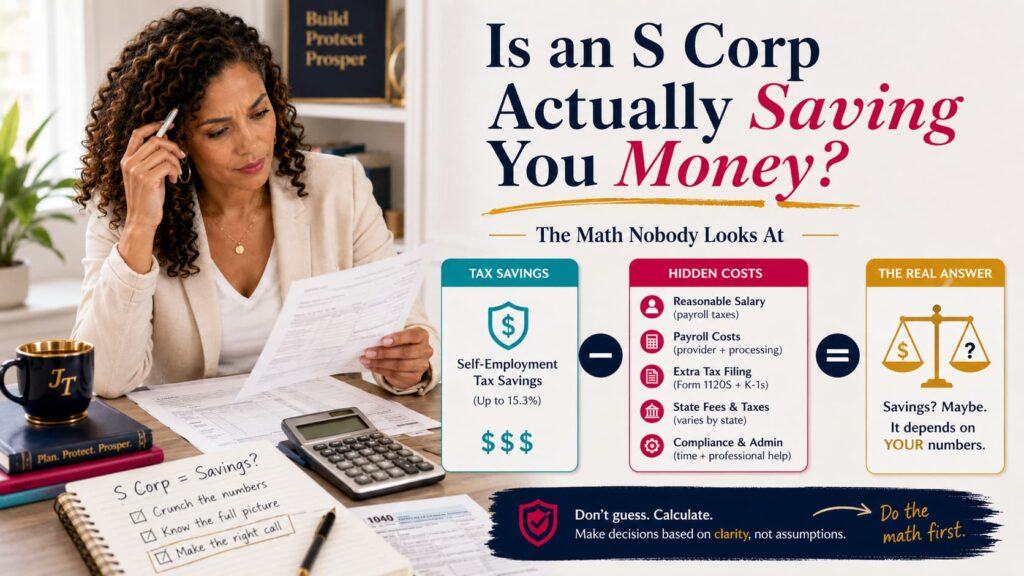

Is an S Corp Actually Saving You Money?

(The Math Nobody Looks At)

Thinking about switching to an S Corporation for tax savings?

Before you make the leap, it’s critical to understand the hidden costs most business owners never hear about. In this guide, I’ll uncover the lesser-known downsides of electing S Corp status so you can make the most informed financial decision for your business.

What you’ll learn:

- The overlooked expenses of S Corps (bookkeeping, payroll, and compliance)

- Why an S Corp may not be right for everyone

- What income level actually makes the switch worth it (and why it’s different for each person)

- How to avoid IRS red flags when paying yourself a salary

- When it’s time to consult a tax pro or financial advisor

Want personalized, step-by-step help? Grab your seat for my free S Corp Switch Masterclass

Got questions? Submit yours for our next Power in Numbers Live Show

S Corp 101 (Super Quick)

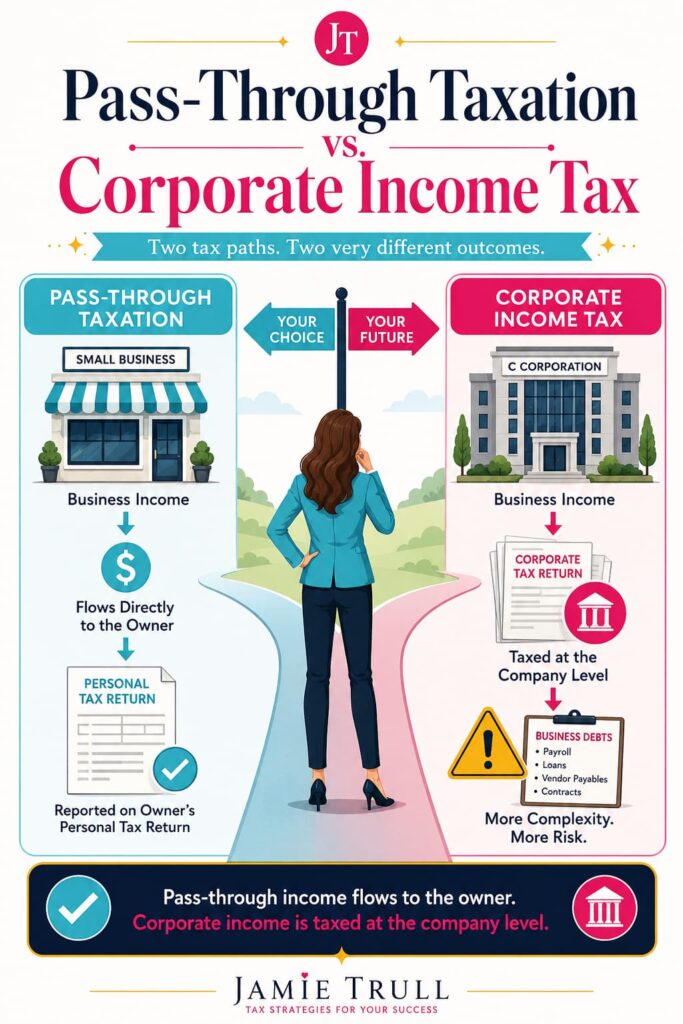

An S Corporation isn’t a business entity. It’s a tax election.

Most small business owners create an LLC and then file to be taxed as an S Corporation.

The potential win is that instead of paying self-employment tax on all profit (like a Schedule C sole prop), you pay yourself a reasonable W-2 salary (subject to payroll taxes) and take the remaining profit as distributions (not subject to SE tax).

That’s the highlight reel.

But behind the scenes are systems, filing annual reports, fees, and rules that can quietly eat into those savings … unless you plan for them.

Hidden Cost #1: Payroll Setup & Ongoing Maintenance

If you’re an S Corp owner, you must run payroll for yourself. That means:

- Selecting a payroll provider

- Withholding and remitting federal and state payroll taxes

- Filing 941/940, state returns, and annual W-2s

- Setting and documenting a reasonable salary

Typical annual cost: $300–$1,200+ (software + filings). More if you operate in multiple states or add HR/benefits.

Make this painless:

- Use a payroll platform built for small teams and first-time S Corps. I recommend OnPay or Gusto for automation, compliance, and clarity.

- Compare my vetted payroll picks (& snag deals)

- Unsure how much to pay yourself? Get my step-by-step Savvy S Corp Salary training

Hidden Cost #2: A Separate, More Complex Tax Return

S Corps file Form 1120-S and issue Schedule K-1s to shareholders.

It’s more involved than a Schedule C, and most business owners hire a pro.

Typical prep fees: $750–$2,000+ depending on state, complexity, and bookkeeping quality.

Pro tip: Clean, monthly-closed books can cut prep costs dramatically.

Tooling up helps:

- Choose accounting that matches your workflow (My comparison + best deals: QuickBooks, Xero, or FreshBooks).

Hidden Cost #3: State-Level Fees & Compliance

S Corps don’t bypass state costs. Depending on where you operate, you may face:

- Annual report fees or franchise taxes (e.g., CA has an $800 minimum)

- Registered agent fees

- Publication requirements (some states)

- Additional S-election paperwork at the state level

Action step: List your state’s annual costs before switching so you can include them in your break-even math.

Hidden Cost #4: Owner Education & Ongoing Rules

S Corps are not “set it and forget it.”

To stay compliant (and maximize savings), you must:

- Set and document a reasonable salary (review yearly)

- Keep true double-entry books (including a balance sheet)

- Track shareholder basis annually (so your distributions stay non-taxable)

- Observe corporate formalities per your state

Skipping these is how avoidable problems become costly ones.

Hidden Cost #5: The Accountable Plan (Reimbursements)

S Corps require a formal Accountable Plan to reimburse you for business expenses you paid personally (home office, phone, internet, mileage, etc.).

Without it, reimbursements can be treated as taxable wages.

Fix: Adopt an Accountable Plan template, require receipts/mileage logs, and reimburse regularly.

Hidden Cost #6: Owner Fringe Benefits (Special Rules)

2% S Corp owners have unique treatment for:

- Health insurance (generally must flow through payroll/W-2 properly)

- Section 125 cafeteria plans and HSA eligibility (limitations apply)

- Other fringe benefits (e.g., vehicle use) may have different tax treatment

A great payroll system + a knowledgeable tax pro keeps this tidy.

Hidden Cost #7: Retirement Plan “Math”

S Corps can supercharge retirement … but your salary controls the limits.

- Solo 401(k): Employee deferrals and employer contributions are calculated from W-2 wages (not distributions). Too-low salary = limited retirement savings.

- SEP-IRA: Employer-only; also based on W-2 wages for S Corp shareholders.

Takeaway: Chasing the lowest salary can backfire if it forces you to save less for the future.

Hidden Cost #8: Workers’ Comp, Unemployment & Multi-State

Your W-2 wages drive state unemployment and may affect workers’ comp.

If you work or hire in multiple states, expect more registrations and filings.

Your payroll provider will help, but it’s still on you to plan for the extra costs and timelines.

Hidden Cost #9: Bookkeeping Uplevel (Time + Tools + Pros)

S Corps require cleaner bookkeeping than a Schedule C:

- Accurate balance sheet (payroll tax payables, loans to shareholders, retained earnings)

- Basis tracking aligned with tax prep

- Consistent owner distributions tracking

DIY is possible … but if books are going to sit, hire a pro to close monthly. You’ll save far more at tax time.

Get my software picks & discounts.

Hidden Cost #10 (The One Nobody Mentions): Timing & Cash-Flow Drag

This is the big surprise.

Even when your total taxes drop, an S Corp can feel tighter because the timing of cash outflows changes:

- Payroll + payroll taxes now leave your account every pay period

- Income tax estimates are still due quarterly on pass-through profits

- You can’t “skip” payroll when cash is light

If you don’t restructure your bank accounts and cash cadence, the S Corp can create cash-flow squeeze stress.

How to fix it (my favorite system):

- Separate bank accounts: Operating, Owner’s Pay, Taxes, Payroll, and Profit/Reserve

Easy multi-account setup with automation (Relay—$50 once approved and funded; offer subject to change) - Automate transfers every time you get paid (percentage-based).

- Build a 1–2 month payroll buffer so you’re never scrambling.

- Create your PROFFIT Plan™ to pre-allocate every dollar with intention.

Is an S Corp Actually Worth It?

Often, yes—when:

- You have consistent profits (not just a one-off spike)

- You can pay a reasonable salary and still have leftover profit

- You’re willing to invest in payroll, clean books, and a tax pro

- You’ll follow the rules (Accountable Plan, basis, etc.)

It may not be the right season if your income is volatile, you’re just getting started, or you’re not ready for the admin lift.

Waiting 6–12 months to stabilize profits can be the smarter (and less stressful) play.

Not sure where your break-even is?

Walk through real-world scenarios in my free S Corp Switch Masterclass.

Quick Decision Framework (10 Questions)

- Are your net profits consistent for 3+ quarters?

- After paying yourself a reasonable salary, will there still be profit for distributions?

- Do you have $300–$1,200+/yr budgeted for payroll software/filings?

- Can you afford 1120-S tax prep ($750–$2,000+) each year?

- Have you researched state fees (franchise tax, annual reports)?

- Will a lower salary constrain your retirement savings goals?

- Do you have a Payroll buffer (1–2 months) and a Taxes account?

- Do you understand Accountable Plan reimbursements?

- Will you keep monthly books (or hire it out)?

- Do you have a pro you can email when you’re unsure?

If you answered “yes” to most of these, S Corp is likely a fit. If not, consider waiting, or get help implementing the systems first.

Your First 90 Days as an S Corp (Checklist)

Weeks 1–2

- Elect S Corp (federal + any state filings)

- Choose payroll provider & set pay schedule

- Open separate bank accounts (Owner’s Pay, Taxes, Payroll, Profit/Reserve). Banking that makes this easy

- Adopt an Accountable Plan policy

Weeks 3–6

- Document reasonable salary (and your method)

- Connect accounting software (get my deals!) ; categorize YTD activity

- Set automatic transfers (Owner’s Pay / Taxes / Profit)

Weeks 7–12

- Reconcile books monthly (bank + payroll + credit cards)

- Run first quarterly projections (income tax + cash)

- Revisit salary and payroll tax cadence if needed

Common Myths vs. Facts

Myth: “I can choose any salary I want.”

Fact: It must be reasonable based on role, duties, and market comps… and documented.

Myth: “Distributions are tax-free.”

Fact: Distributions avoid self-employment tax, but profits still create income tax (and you need basis to keep them non-taxable).

Myth: “I switched to an S Corp, so I won’t need quarterly estimates.”

Fact: You’ll still likely pay quarterly income tax on pass-through profits.

Myth: “I can reimburse myself however I want.”

Fact: Without an Accountable Plan, reimbursements allows for treatment as taxable wages.

FAQs

What income level makes S Corp “worth it”?

It’s case-by-case. When you can pay a reasonable salary and still have meaningful profit for distributions after costs (payroll software, tax prep, state fees), it often pencils out. We model this in the masterclass.

Can I switch back if I regret it?

Possibly, but it has timing rules and admin costs. Better to decide thoughtfully up front.

Do I have to be an LLC to elect S Corp?

You need a legal entity (LLC or corporation) to make the S election; sole proprietors can’t elect S Corp directly.

Will this affect Social Security?

Potentially. Lower salary = lower payroll tax paid in = could reduce future benefits. Plan retirement accordingly.

Final Word

An S Corp can absolutely save you money—when it’s done right. But those “invisible” costs are real: payroll, state fees, clean books, compliance, and cash-flow timing. Go in eyes wide open, build the right systems, and your S Corp can become a powerful part of your long-term strategy.

Ready to see if the numbers work for you? Join my free S Corp Switch Masterclass

Have questions? Submit them for our next live Q&A!

Disclaimer: This article is educational and not tax, legal, or financial advice. Talk to your tax advisor about your specific situation.

Transcript

S Corp Benefits vs LLC: Hidden Costs and Tax Savings

Everyone loves to talk about how an S corp can save you thousands in taxes, but what are they not telling you? There are hidden costs that can surprise you if you're not prepared, and they can eat into those tax savings pretty fast Hi, I'm Jamie Trell, your favorite CPA and financial literacy educator, and on this channel I like to bring you all the resources to keep you informed, organized, and profitable in your business finances, so please make sure to like and subscribe.

And if you're a business owner or freelancer or solopreneur, maybe even a side hustler, and you're thinking about becoming an S corp, this video is gonna help give you the information you need to make that decision. Plus, stick around to the end because that's when I'm gonna share the most hidden small things that nobody seems to talk about when it comes to an S corp that a lot of people don't realize until after they've already done it.

S Corporation and Tax Classification

But first, let's start with a quick refresher. Now, an S corporation isn't actually a legal entity, it is a tax election. And that tax election ultimately allows you to take the money that you make in your business and be able to divide it into two buckets: one bucket, which is your salary, that gets fully taxed; and one bucket that is distributions that does not have self-employment taxes on it.

So that's generally where the savings of an S corp come in and why a lot of people recommend going that route, especially once you make a certain amount of money. Now, just to interject, there isn't a very specific line here of when it makes sense to become an S corp. I usually tell people to start looking at it maybe roundabout when they're making at least $70,000 in profit or more.

So tax savings sounds great. Who doesn't want that? But you wanna make sure that you do it right. And this is the thing that many people gloss over, and many professionals even gloss over, is that there are hidden costs to becoming an S corp. It is not free to do it. So you need to make sure that if you're calculating those tax savings, you're also accounting for the fact that there will be added costs.

Reasonable Salary and Payroll Costs

So let's talk about the most obvious cost first, and then we're gonna get to the more hidden ones at the end of this video. So the first more obvious cost is payroll. If you are now needing to be an employee of your business, which is a requirement of S corp, you do need to pay yourself a reasonable salary.

If you don't know anything about this, I have lots of content all about determining your reasonable salary. But you're likely going to want to have a payroll provider to make sure that all of your taxes are getting withheld properly and all of those payroll forms are being filed appropriately with the IRS.

Now, that's not something that you have to do if you are a sole proprietor or single-member LLC because you just get to take distributions from your business when you have the money. But this is an added cost. Now, in the grand scheme, payroll providers aren't overly expensive for what they do, especially if you use one of the ones that I recommend.

Definitely go check out jamietrell.com/payroll. I also have special deals with many different payroll providers. However, it can add up. So typically you're gonna look at paying anywhere between $300, maybe even up to a $1,000 depending on the provider you use to just run your payroll and manage that process for you.

Small Business Tax Treatment and Additional Filing

Now, if you're already running payroll because maybe you already have employees and so this would just be adding yourself, it may be less expensive. But if you are your only employee, then this- Probably going to be a little bit more of a cost for you. Now again, if you wanna check out some of the payroll providers that I recommend, definitely watch this video next.

Now, the second not quite as hidden cost is additional tax filing. So there will be another tax filing instead of just filing your 1040, which typically if you are a single member LLC or a sole proprietor, you would just add a schedule into your normal annual tax return, your 1040. In this case, you're gonna have an extra tax return called an 1120S, and it's due a month before that April 15th deadline.

And because this is a corporate return, it often is going to cost more than just a normal 1040 might cost you to be able to file. So typically, you're gonna see this range from anywhere from about $750 for someone to file it up to a few thousand dollars. And even if you DIY your current taxes, if you use TurboTax or something like that for your personal taxes, I highly, highly, highly recommend hiring someone to do your taxes for you as an S corp, at least your corporate tax return, because it is trickier, and doing it wrong can lead you down a road where you might end up with penalties and fines or just back taxes that you have to pay.

Business Structure and State-Level Compliance

Okay, so now we're getting into some of the more hidden costs, but these are important. So the third hidden cost is state-level fees and compliance. T

his very much varies based on the state that you are in, but it can be more costly in certain states to be an S corporation, and that can eat into some of these federal self-employment tax savings.

So for example, in the state of Tennessee, where I live, there is a franchise tax, and that franchise tax is only going to apply to any earnings that I have that did not previously have payroll taxes taken out of it.

That means the state is going to add extra taxes on top of what I'm paying federally, and that's something that needs to be considered as well.

Also, in states like California, just to have an LLC, which remember, you do need to have an entity in order to elect S corp taxation, so you would need to be, say, an LLC in order to do it. In the state of California, just to have an LLC, it's $800 minimum every single year, and that's even if you're not making any money.

So that's why it's really important to get to know your state rules and see if any of those tax savings federally are gonna be offset by additional costs with the state, and then you can factor that in when you're making your decision.

Corp Status and Owner Education

And the fourth cost is gonna be owner education and compliance. So at the end of the day, even if you do hire someone, you are responsible for doing things the correct way.

Unfortunately, S corp is not a set it and forget it thing. You are the one who's gonna be responsible for many things, such as making sure that your pay is considered reasonable with the IRS, keeping track of separate- And accurate financial statements, including a balance sheet. So previously you may not have needed a balance sheet.

If you are an S corp, you are gonna wanna have full financial statements including a balance sheet. And you're also gonna need to track what's called your basis in the business. That's essentially your owner equity in the business. And the reason that that matters when you're an S corp is that if you end up taking distributions from your business that are in excess of what's considered your basis, then you may inadvertently end up taking taxable distributions.

So again, there's more things to pay attention to, more things that can go wrong, more things that can trigger additional taxes if you're not on top of it.

Now I'm gonna get into some of the … So now I'm gonna get into the even deeper hidden costs. And some of these are ones that are harder to put a dollar amount to, but they are things that you need to be aware of.

Limited Liability Company and Family Business Costs

So for example, I talk a lot on this channel about the tax strategy of hiring your minor kids. I'm a big fan of it. Done correctly, hiring your children offers a great way to shift income from a higher tax bracket, yours, to a lower tax bracket, your kids. However, if you've watched my content on this, you know that it gets more difficult when you are an S corp to hire your kids.

There are gonna be more rules, more things that you need to do. You can still make it happen. But it isn't quite as easy and straightforward and there is some additional cost to it versus if you were to hire them from an LLC or a sole proprietorship. So if you wanna have a family business, that's something to definitely keep in mind.

It may not be a reason not to do it, but you just wanna be aware. And another big one that trips a lot of people up is the change in how your own out-of-pocket expenses are handled. So if you have business expenses that you as the owner are paying on your own behalf, let's say your business, you're using your phone 50% for business.

Tax Treatment and Accountable Plans

Typically, if you were an LLC or sole proprietor, you could give that to your accountant, they would just add it to your Schedule C, no big deal. But it's very different when you are an S corp. You actually have to have a more formalized plan, which is called an accountable plan. It's basically a reimbursement plan.

But it basically spells out what you get reimbursed for, and that's how you need to be reimbursing yourself and that makes sure that then any distributions you're taking don't end up becoming taxable. And that allows them to still be able to write them off for your business and reduce your total taxes.

So you wanna be really aware of that. That's something that can trip people up and it can create additional taxes if they're not doing it correctly. Now another hidden hidden cost to consider is that Being an S corp can impact the amount that you are able to put into your retirement accounts. It really depends on the type of plan you set up, but you may now be limited in the calculation of your total maximum you can put into a retirement account, like a SEP account, based on your salary, and therefore that could actually reduce the amount of contributions you can actually make.

Pass Through Entities and Social Security Considerations

It really depends, and it can vary based on your situation, but again, something to keep an eye on. And the last thing to keep in mind as well that I like to make sure people remember is the fact that if you are paying less in Social Security and Medicare, i.e., those are also called payroll taxes or self-employment taxes, right?

That's what we're saving on with an S corp. Well, if you're paying in less Social Security, then that means later on your benefits that you're getting from Social Security may be reduced. So that's something to know and to think about. I typically don't consider that a game changer because, again, you're getting more money now, right?

So if you were to take that money and invest it for your future or put it into a retirement account, right, that's probably gonna be better than relying on those Social Security benefits anyway. But it's just something to be aware of that if we pay in less to Social Security, that may mean our Social Security benefits down the line are reduced.

Key Differences in S Corp vs LLC Decisions

After all that, I know I sound like a Debbie Downer, is being an S corp even still worth it? And I would say that for many business owners, yes. My main business is an S corporation because it does make sense for me, and it does save me money overall. However, I went into it eyes wide open and made sure to consider all the things I've talked about today when making that decision.

So if you want to delve into this a little bit more and see if it might make sense for you to be an S corp, I go into more detail in my S Corp Switch masterclass. It is a workshop where I walk through exactly when you might want to shift and some of the considerations around it. So if you're interested, definitely go check that out at jamietrull.com/switch.

And also make sure to subscribe because I have lots of content on this channel all about being an S corp and making sure that you follow the rules and you're paying yourself that reasonable salary. Thank you so much for watching, and I'll see you next time.

Stop Guessing and Get the S Corp Blueprint Your Accountant Left Out

The Takeaway: Ready to pull back the curtain on the actual compliance costs?

Download the S Corp Toolbox for plain-English guidance and interactive calculators designed to protect your hard-earned cash.