You’re booking clients.

Revenue is growing.

But your bank account is still whispering “nope.”

If that sounds painfully familiar, you are not alone.

The truth? Revenue ≠ profit, and profit ≠ cash in the bank.

Until you build a simple, reliable cash management system, your business will always feel like a high-stress juggling act—no matter how big the top-line number gets.

In this definitive guide, we’ll break down why money vanishes between sales and your checking account, the most common blind spots keeping entrepreneurs feeling broke.

Plus, how to install a cash flow system that pays you first and funds what matters—on autopilot.

Your challenge, should you choose to accept it:

• 📈 Create your PROFFIT Plan™ (free template)

• 🏦 Set up Relay for envelope-style business banking (+ $50 bonus once funded)

• 📊 Download my Cash Flow Worksheet (weekly forecasting)

• 📘 Order Hidden Profit + get $300+ in bonuses

Disclaimer: this post is sponsored, but as always—we’re only sharing tools and resources we personally use and love. Your support helps us keep showing up and supporting our small (but mighty!) team

*Relay Disclosure: Relay is a financial technology company, not a bank. Banking services and FDIC insurance are provided through Thread Bank, Member FDIC. The Relay Visa® Debit Card is issued by Thread Bank pursuant to a license from Visa U.S.A. Inc. and may be used everywhere Visa® debit cards are accepted.

1) Revenue ≠ Profit ≠ Cash: The Three Numbers You Must Not Confuse

Let’s get clear on definitions most owners never got in plain English:

- Revenue – All the money billed/collected for your products/services.

- Profit – What’s left on paper after expenses (Revenue − Expenses = Profit). This is what you pay income taxes on.

- Cash – The actual dollars in your bank accounts after money moves (timing matters!).

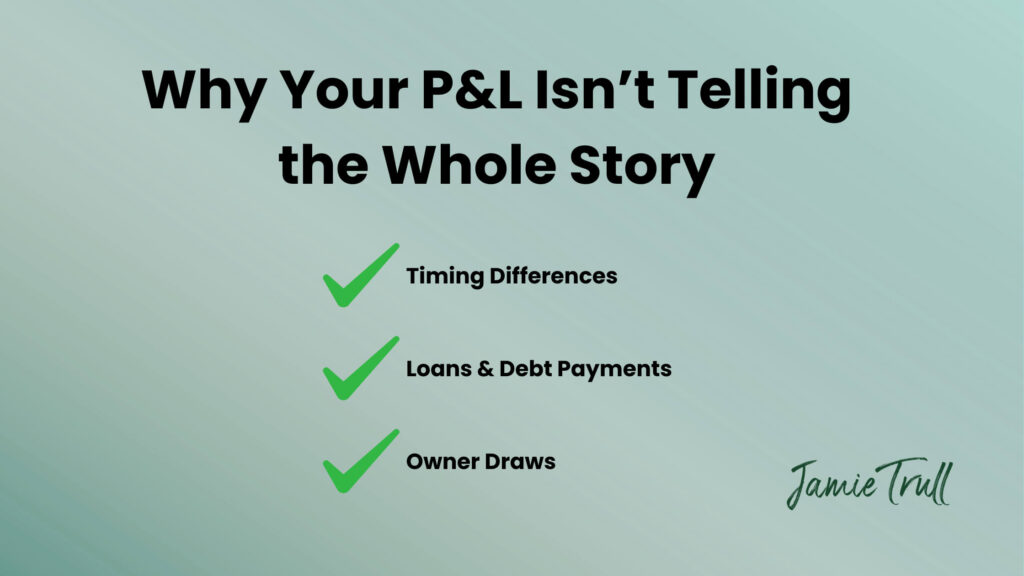

You can be “profitable” and still struggle to make payroll or pay yourself. Why? Because profit includes accounting timing and non-cash items. Cash measures what actually happened.

The Leaky Bucket Analogy

Imagine your business as a bucket. Water in = revenue. Holes = expenses, debt principal payments, inventory purchases, taxes, and owner draws. If the holes are big enough, increasing the faucet (more sales) won’t help—you still end up empty. First, patch the holes. Then, turn up the faucet.

2) Where Your Money Is Disappearing (Even When Sales Look Good)

Here are the seven most common profit-to-cash disconnects—and how to spot each one fast.

A) Accrual Timing vs. Cash Reality

- On accrual accounting, you record revenue when earned and expenses when incurred, not when cash moves.

- Result: Your P&L says “profit,” but your bank says otherwise because invoices aren’t collected yet or bills haven’t been paid.

Spot it: Growing Accounts Receivable and Accounts Payable balances, even when P&L looks healthy.

Fix it: Shorter payment terms, deposits/milestones, automatic reminders, and accepting online payments.

B) Inventory Is Eating Your Cash

Buying inventory doesn’t hit your P&L as an expense until it’s sold (COGS). But cash leaves now.

Spot it: High inventory purchases, slow turnover, frequent “sold out” or “overstocked” cycles.

Fix it: Forecast demand, tighten reorders, clear dead stock, raise prices where margin is too thin, and earmark opportunity funds for strategic buys (more on this in PROFFIT Plan).

C) Debt Principal Payments Don’t Reduce Profit (But Do Reduce Cash)

Only the interest hits your P&L. The principal is a balance sheet item—yet it drains cash each month.

Spot it: Loan statements showing big principal payments while your P&L understates total outflow.

Fix it: Build these payments into your weekly cash forecast and set aside funds ahead of due dates.

D) Owner Draws Are Not Expenses

Distributions/draws don’t appear on your P&L. You can look profitable but be cash-poor if you withdraw ahead of true capacity.

Spot it: Positive profit + low bank balance + significant owner distributions.

Fix it: Switch to a fixed owner’s pay (see PROFFIT Plan), and increase it only when margins support it.

E) Subscription Creep & Overhead Bloat

$29 here, $79 there—over 12 months and multiple tools, it’s thousands. And many are not ROI-positive.

Spot it: A long list of small recurring charges in your bank feed.

Fix it: Quarterly subscription audit: cancel, downgrade, or consolidate tools. Use Relay to see recurring charges clearly.

F) Generous (and Unstructured) Client Terms

No deposits. Net-30 that turns into Net-45/60. No late fees, no reminders, no auto-billing. That’s a cash flow killer.

Spot it: Rising DSO (Days Sales Outstanding).

Fix it: Standardize terms: deposit upfront, milestone billing, Net-7/14 on remaining, auto-reminders, and late fees. If work is ongoing, use recurring auto-billing.

G) Tax Season Shock

You’re profitable and then—surprise—quarterly estimates and year-end taxes drain the account.

Spot it: Scramble each quarter (or every April).

Fix it: Automate tax set-asides every deposit. Don’t “borrow” from the tax bucket. Ever.

3) The Simple System That Stops the Bleeding: The PROFFIT Plan™

If you’ve heard of Profit First, PROFFIT Plan™ is my flexible, goals-driven spin that maps every dollar to a purpose you actually care about. The letters stand for the funds you’ll maintain:

- P — Pay Yourself (Owner’s pay)

- R — Rainy Day (operating buffer / emergencies)

- O — Opportunity (growth investments: team, ads, education, launches)

- F — Future (debt paydown & retirement)

- F — Fun (motivation fund: trips, remodels, rewards)

- I — Impact (giving/philanthropy)

- T — Taxes (federal/state/SE)

Instead of letting expenses devour everything, you pre-decide percentages for each bucket (and adjust seasonally). Every time money lands, you split it into these funds. The magic is consistency.

👉 Get my free PROFFIT Plan™ template: jamietrull.com/PROFFIT

4) Put Your Plan on Rails with Relay (Bank Buckets & Automation)

To make this effortless, I use Relay (a Profit-First-friendly business banking platform) to open multiple checking accounts—one for each PROFFIT fund—and then automate transfers based on percentages. You can even create rules like “any amount over $X in Operating sweeps into Tax, Pay Yourself, Rainy Day, etc.”

Why Relay works so well:

- Open up to many accounts with unique account/routing numbers.

- Clear visibility: no more “mental buckets”—they’re real.

- Easy automation: set it once, let it run.

- Great for cash discipline: money for taxes can’t be accidentally spent.

🏦 Start with Relay (+ $50 when you fund)

5) Your Weekly “Money Monday” Routine (15–20 Minutes)

Consistency beats intensity. Every week, run this simple cadence:

- Update your Cash Flow Worksheet (8–10 weeks out):

- Expected inflows (by client, by date)

- Outflows (subscriptions, payroll/contractors, debt payments, taxes, one-offs)

- Spot shortfalls 2–4 weeks ahead—when you still have options.

- Expected inflows (by client, by date)

- Run allocations (according to your PROFFIT percentages).

- Collect faster: send/auto-send invoices, reminders, and apply late fees per policy.

- Review AR: call or email on any invoice > 14 days overdue.

- Trim: cancel or downgrade any subscription you didn’t use last week.

📊 Grab the Cash Flow Worksheet.

6) Numbers That Tell You the Truth (Mini KPI Dashboard)

- Gross Margin % = (Revenue − Direct Costs) ÷ Revenue

Is the core work profitable? Target improves as you refine pricing and delivery. - Overhead Rate = Overhead ÷ Revenue

Are the “everything else” costs ballooning? - Operating Profit Margin = (Revenue − Direct Costs − Overhead) ÷ Revenue

Healthy ops margin = capacity to pay yourself and reinvest. - Owner’s Pay % = Owner Pay ÷ Revenue

If this is near zero, your system is paying everyone but you. - DSO (Days Sales Outstanding) = (AR ÷ Average Daily Sales)

Higher DSO = your clients are using you as a free bank. - Cash Runway = Cash ÷ Average Monthly Net Outflow

How many months can you keep the lights on without new sales?

Watch these monthly. Adjust pricing, terms, and costs to drive them in the right direction.

7) Pricing That Actually Covers Your Role

One silent killer: pricing as if you’re an employee, not the owner. Your rates must cover:

- The market value of labor required to deliver (even if it’s currently you)

- Overhead and tools

- Owner profit for the risk you take

- Taxes

If you “couldn’t afford” to hire someone to replace parts of what you do, your pricing is too low. Raise rates or re-scope offers until your gross margin and owner’s pay make sense.

8) The Collections Playbook (No More Waiting 60–90 Days)

Standardize this once—watch cash flow smooth out:

- Deposits: 25–50% at booking for projects.

- Milestones: Tie payments to deliverables, not vague dates.

- Terms: Net-7 or Net-14 for services (Net-30 is optional, not default).

- Auto-billing: Save cards on file for recurring work.

- Reminders: 3 days before due, on due, 7 days late, 21 days late.

- Late fees: After a grace period (e.g., 10 days), apply a % or flat fee.

You’ll collect faster—without ever writing a “just circling back” email again.

9) Fast Growth Can Make You Feel Broke (Here’s Why)

Counterintuitive but common: rapid growth often creates cash pressure. You hire ahead of collections, buy inventory before revenue catches up, and stretch delivery capacity. That’s a timing gap, not a failure.

What to do:

- Use deposits/milestones to fund delivery.

- Monitor runway and DSO weekly.

- Increase prices and prune unprofitable work.

- Build Rainy Day and Opportunity funds so growth doesn’t starve you.

10) Your 7-Step Profit & Cash Clarity Plan (Do This This Month)

- Create your PROFFIT Plan™ and assign starting percentages.

- Open Relay accounts to match the buckets and set automatic allocations.

- Install Money Monday—use the Cash Flow Worksheet weekly.

- Raise your collection standards—deposits, milestones, auto-billing, and late fees.

- Audit subscriptions—keep only what saves time or makes money.

- Re-price any under-margin services—especially time-intensive offers.

- Pay yourself every month—even if it’s small to start. Build the habit now.

Final Word: You Don’t Need to Earn More—You Need a System

The belief that “more sales will fix it” is the burnout trap. More water won’t help a leaky bucket. Fix the leaks with a simple, automated plan that pays you first, funds your goals, and keeps taxes/timing from blindsiding you.

You’ve got this—and I’ve got the tools to make it easy:

- 📈 Build your PROFFIT Plan™ (free): jamietrull.com/PROFFIT

- 🏦 Use Relay to implement it (+ $50 when you fund): jamietrull.com/relay

- 📊 Run your weekly forecast (template): JamieTrull.com/cashflow

- 📘 Go deeper in my book—Hidden Profit (pre-order + bonuses): JamieTrull.com/HiddenProfit

Transcript Disclaimer: This transcript was generated from the video for your convenience, but it may contain typos or slight errors due to the transcription process. For the most accurate and complete information, we recommend watching the full YouTube video.

Why You Feel Broke in Business Even With High Revenue (revenue vs profit, owner’s pay)

Your booking clients, your revenue is growing, but your bank account still says, Nope. Sound familiar? You’re not alone. And today we’re unpacking why that might be happening and how to fix it.

Hey y’all. I’m Jamie Trull, your favorite CPA and profit strategist.

And here on this channel I like to bring you all the content to keep you informed, organized, and profitable in your business. So please make sure to like and subscribe. And if you feel like you’re doing everything right in your business, but you still feel broke, this video is for you.

And make sure to stick around until the end, because I’m gonna tell you the biggest mindset trap that keeps entrepreneurs in that cycle, and that one little shift could make all the difference.

So one main reason you may feel broke in your business, even though money is coming in, is the very, very simple equation that revenue does not equal profit, right?

Revenue, IE, the money coming into your business is different than what is actually left over to pay yourself. And just because money is coming in, it does not mean that it’s staying.

The Myth of High Revenue and the Reality of Profit Margins

Now, I feel like in this day and age we’re inundated with all these messages of these businesses that seem to be doing so great. They’re talking about being a seven figure, eight figure, nine figure business. And that might make you feel like you’re doing something wrong. However, the thing that those businesses rarely disclose is what their actual cash profit is. How much is actually available for those business owners to pay themselves at the end of the day? Because those businesses might be bringing in, let’s say, a million dollars. They might actually be a seven figure business, but what if their expenses are $950,000 before paying themselves? That means they’re left with just $50,000. So if you’re a solopreneur without very many expenses making $50,000, you might be doing just as well as someone who’s making a million dollars in revenue. Revenue does not equal profit and revenue does not necessarily make for a healthy business. Now, obviously, you need revenue in a business. I’m not saying you can have a business without it, right? There’s no money flowing in. It’s not really a business. But the second part of that profit equation is expenses.

Understanding Costs That Hurt Your Profit (gross margin, cost of goods sold, overhead costs)

Right. Revenue minus expenses equals profit.

Profit is what tells you what you can pay yourself as an owner, okay? If you’re spending all your money in your business, and when I talk about expenses, I’m not including owner salary in there.

Just to clarify, if you are spending all your money in your business before you pay yourself. You are not gonna have much leftover to actually compensate you for the work you’re putting in.

So there’s a lot of different things that could make it such that you don’t have much leftover at the end of the day.

Direct Costs, Pricing, and Gross Margin Problems

First and foremost, you might have high direct costs.

So those are things that are specifically related to the good or service that you’re selling. So think of it as the cost of good sold, right? If you’re buying and reselling products, that’s the wholesale price that you’re paying.

If you’re in a service business, that’s the value of your time or your team’s time. So if you don’t have high enough gross profit margins, right, that’s gonna be your revenue minus your direct costs, then that’s going to be an issue for you.

But oftentimes, business owners are a little bit better at tracking those direct costs and making sure that they’re pricing appropriately to make sure that they have some margin.

Hidden Overhead Costs and Subscription Creep

However, where you might get hurt. Is on all of those indirect costs. Those are costs that you can’t necessarily attribute to a specific product or service.

Sometimes you might have heard them referred to as overhead costs. So these are kind of the extras, right? The office supplies the software that you’re paying to service all of your customers, right?

Or to schedule your phone calls or whatever it is. Your admin assistants that you can’t necessarily divide their time out between your clients, right?

All of that is kind of this overhead, indirect expenses, and that’s oftentimes where things can balloon out of control.

And oftentimes the other thing that happens is that we reinvest all of the money in our business, right?

If you’re running a business with inventory and you are making money, and then it feels like you’re just using that money to buy more inventory, right?

That can create this cashflow crunch.

So there are lots of reasons that we could be in a situation where your revenue might be good and growing, but your profit isn’t keeping up.

Fixing Profitability With a Cashflow System (Profit First, PROFFIT Plan, envelope budgeting business)

So how do we fix this problem?

Well, I want you to think of your business as a bucket.

Okay? Stick with me here.

So your business is a bucket, and you’ve got money that is coming in.

So that’s everything. That’s the water that’s coming into the bucket. Is the money coming in? All right.

Now what happens if you have a bunch of holes in the bottom of your bucket?

Those are your expenses.

The Leaky Bucket Analogy for Business Finances

Now, if you have teeny tiny holes, not as big of a deal, it’s gonna just, you know, maybe a little bit’s gonna drip through.

But if you’ve got these big gaping holes, you’re not gonna be able to hold on to much of that money, right?

It’s just gonna go straight on through.

So even if you were to increase the amount of money you make, IE increase the amount of water going into the bucket, it’s still eventually all going to drain out.

So we need to fix those holes.

How Profit First and Profit Planning Create Structure

So what’s one way to fix this problem?

Well, you want to institute a cashflow system, and that might be something like Profit First. It’s a book by Mike Malowitz, it’s very popular.

It’s a way of dividing your money into different buckets.

I have my own, but a little bit of a different take on profit.

First, I do what’s called profit planning. It’s my own signature method of managing my cash.

You can check out more about that, but what I like about it is that it also helps you save up to reinvest back in your business.

You can save for your future; you actually have money that’s set aside just to save for things that are fun, right? It’s a little bit broader than what Profit First does.

But whatever you do, ultimately it’s gonna be important to divvy up your money into different buckets and then not touch the money that is for something else.

Paying Yourself First Using Better Banking Tools (Relay, owner’s pay, budgeting buckets)

So whether that means it’s money that you set aside to pay your taxes or to pay yourself, you aren’t dipping into that to pay your ongoing bills, and that may force you to figure out ways to save money on those bills, right?

We don’t wanna pay ourselves last. We want to be a priority in our business.

You wouldn’t work for somebody else for free.

Why would you work for yourself for free?

So make sure that you have a cashflow system that will pay you.

Separating Taxes, Bills, and Paychecks With Cash Buckets

And if you wanna see what I use for this, check out this video next. In this video, I go through how I use Relay Business Banking to separate my money automatically.

So it’s really, really easy to do.

You can set it and forget it if you want to, and it’s going to help you reach those savings goals without dipping into it to pay for bills and making sure that you are paying yourself and setting aside money for the things that are important to you.

Guardrails for Irregular Bills and Inconsistent Income

So I’m always a big fan of using tools to help you. This doesn’t have to be all up to you. You don’t have to do all of this manually, so find the tools that exist out there.

Relay is a great one to start with if you don’t have anything like that, and utilize that to kind of put the guardrails in place so that you can reach those goals. Now, the other thing that can become an issue, even when you set up a proper plan where you’re setting aside money.

It’s those irregular or unexpected bills that come up that can really throw you for a loop. So add that to the fact that a lot of businesses have inconsistent income, and if your expenses also aren’t consistent, what are you supposed to do then?

How to Use a Cashflow Forecast to Plan Ahead (cashflow forecast template, recurring expenses)

So again, I wanna talk about my profit planning because it allows you to save for a rainy day.

That’s the R in profit, and it allows for you to save. For reinvesting back into your business when things happen, maybe when you want to take advantage of an opportunity that’s really great.

You wanna buy a new educational program, you wanna hire someone, whatever it is, you have the money set aside to be able to do that, and you don’t have to dig into your normal daily expense budget.

To pay for those things, right?

Building Savings for Rainy Days and Reinvestment

So definitely go to jamietrull.com/profitplan. That’s where you can actually pick up my free spreadsheet that actually helps you create your profit plan.

And there’s even a video tutorial that goes with it that shows you how to do it and how to think through how much you want to put in each of these different buckets and what types of things you should be saving for.

And then, like I said. Relay business banking or something like that can be really great to be able to implement your profit plan.

Forecasting 8–10 Weeks Ahead to Avoid Cash Crunches

Now, the other thing that I would recommend you do, just so that you have line of sight on some of these things is to actually sit down and do a cashflow forecast.

And I’m not talking about a cashflow statement.

A cashflow statement is looking backward.

A cashflow forecast is looking forward. It is looking at what is coming.

So I typically do that. Weekly, I look about eight to 10 weeks into the future, and I think about each week how much revenue do I expect to come in, and what expenses do I expect to go out the door.

And so I can look and see like, okay, well my insurance payment is happening that only happens once every six months and that’s coming out three weeks from now.

So instead of that surprising me and all of a sudden I don’t have enough money to pay myself.

Why Fast Growth Can Make You Feel Broke (scaling costs, accounts receivable, inventory cash traps)

I can put that in the schedule and then I’ll be able to see the full picture of what’s coming. And you can even build in a little bit of buffer too, just to make sure you’re not gonna create a cash shortfall.

Because what happens when all of a sudden we’re surprised is we don’t have the same options that we would have had we known that was coming weeks ago. Right. So right now I have more options.

I can try to bring in more revenue or go collect some outstanding invoices to cover that, I can maybe delay some expenses or try to reduce some of them.

I can change around some of the timing of different things, but flash forward three, four weeks from now, there’s very little that I can do at that point to avoid that cashflow crunch.

And now it means I’m probably going to be reducing what I can pay myself.

Timing Issues Between Payroll and Getting Paid

So that I can handle this cash flow, and I don’t put myself in a bad situation by taking too much money out of my business.

And another reason, and this is a little counterintuitive stick with me, but another reason that you may feel broke in your business, even though revenue is coming in, is that you’re growing really fast.

And again, that sounds counterintuitive, but think about it. Right?

If you are growing really fast, you may have, you know, more and more work to do. You might need to hire more people, you might need to buy more inventory, and you may not actually be getting paid on that until later down the line.

So for example, if you’re a service-based business and you have to hire a few more staff and they’re doing work for clients, let’s say, and then you bill the clients in arrears and then you have to collect on those invoices.

You might have had to pay your staff weeks before you actually make the money from the client. And that can create a cashflow crunch, even though you may have more clients than ever before and your margins might be great, right?

Balancing Growth and Paying Yourself (distributions vs expenses, reinvestment strategy)

So it’s a little counterintuitive.

Similarly, if you are in a business that has inventory and you’re growing and you’re trying to stock up on, I. Then a lot of the money coming in, you’re just reinvesting back into your business to buy more inventory, and it may never feel like there’s actual cash coming out of it.

It’s just this, you know, constant reinvesting. And that’s another reason that it’s really important to set up a profit plan to make sure that you’re carving out enough money to actually pay yourself too.

You need to have that planned in there so that even in the midst of that growth you are being able to reinvest. Yes. But also being able to be compensated for the work that you do.

You don’t wanna keep, you know, sending it down the line.

Say, someday I’ll make money.

Make money now. Right?

Why You Must Pay Yourself Even While Scaling

Take money outta your business.

Now, that doesn’t mean that you don’t wanna reinvest to grow, but. 100%. Uh, growth versus 0% to you isn’t a good formula, right?

At least make it 80 20 or something like that where you’re still reinvesting, but you’re making sure to take a piece of that cut along the way.

You have bills to pay, right?

Unless you’re independently wealthy, you probably need that money.

So make sure to make it a habit because when you don’t, and I’ve seen this happen with business owners. When you don’t make it a habit, you might think, oh, I’ll pay myself.

You know, a year from now when, when things are, uh, better and it will continue to roll.

And there are business owners who I kid you not are like five, 10 years into business and have rarely if ever paid themselves.

And that is shocking to me. Shocking.

The Biggest Mindset Shift for Business Profitability (profit vs revenue, burnout prevention

Maybe they took a little bit of money out here and there, but for the most part it’s all just being reinvested and that’s great and all. But y’all we’re humans.

We got bills like, take pay yourself.

Please, please, please, please, please pay yourself what you deserve.

And I’ll tell you the real trap is thinking that more income equals less stress. We often think that we’re gonna solve this problem just by working more and more and more and making more money coming in.

That is a recipe for burnout unless you have fixed that leaky bucket, right?

So don’t just try to put more in, ’cause you’re just gonna burn out. You’re gonna get exhausted. You’re still gonna feel like there’s not enough left.

At the end of the day, fix those profitability problems first.

Then you can go turn that faucet on and fill up that bucket.

Why Managing Money Beats Earning More

But only then. Which brings me to that mindset shift I mentioned earlier, which is really, really key in all of this, which is that you don’t need to earn more. You need to manage your money smarter.

Now again, if you’re in the beginning of business and you don’t have very many clients and you’re not bringing in much money, okay, sure. You need to focus on going.

Figuring out what are you offering in the marketplace? How do you sell that thing? But if you are making money and still not having enough left at the end of the day, then this is more about managing the money in your business than bringing more money in.

Right? And until we figure out how to manage it well, bringing more in is not going to solve the problem. It’s just gonna burn us out.

Hidden Profit: Finding More Money Inside Your Business (Jamie Trull Hidden Profit)

Now, if you want to get more into the strategy of this, if you’re like, heck.

Yes, I would love to be able to make more money without having to constantly be working more, bringing in more sales that I need you to go and check out my book. It’s my very first book ever.

I would love for you to pre-order it. It comes out officially October 21st of this year. However, it is available for pre-order and pre-ordering is. Huge, huge, huge.

For new authors like myself, it makes a really big difference.

How to Access Bonuses and Resources for Growing Profit Margin

So go to jamietrull.com/hiddenprofit.

There you can see we also have some awesome pre-order bonuses worth over $300 for you to grab just by buying the book. You don’t have to do anything else.

Just buy the book and then come over and tell us you bought it and put in your receipt number and you’ll get all of these bonuses, and I’m super, super excited about them.

And I’ll tell you that my heart and soul went into this book, hidden Profit. It is all about finding the profit that’s already hiding in your business, making little tweaks that can add up and compound to a huge difference in your business and in your life.

So definitely go check it out.

I’m so, so proud of it and I really hope you read it. And also make sure to check the next video, which is Five Places Your Profit might Be Hiding. ’cause that is a great compliment to this video right now.

I’ll see you guys later.